Key Takeaways

- Olo Inc. (OLO) stands at the forefront of restaurant digital transformation, offering a comprehensive SaaS platform for ordering, payments, and guest engagement.

- Despite strong market penetration and a compelling "Guest Data Flywheel" strategy, Olo faces intense competition and significant criticisms regarding its growth projections and financial transparency.

- The company's recent transition to private ownership, facilitated by Thoma Bravo, signals a strategic pivot to accelerate innovation and M&A away from public market pressures.

Is Olo Inc. (OLO) Revolutionizing the Restaurant Industry?

Olo Inc. (OLO) is a pivotal player in the ongoing digital transformation of the restaurant industry, providing a software-as-a-service (SaaS) platform that enables multi-location restaurants to manage on-demand commerce operations. The company's core mission revolves around empowering restaurants to build lasting relationships with guests, create frictionless experiences, and leverage data-driven insights to stay competitive. As the industry navigates evolving guest expectations and persistent cost pressures, Olo's integrated solutions aim to streamline operations and enhance customer engagement, whether through online ordering, delivery, or in-store interactions.

The shift towards digital solutions is not merely a trend but a fundamental recalibration of how restaurants operate. Olo's platform addresses critical industry "outs" for 2025, such as forced service models, friction-filled guest experiences, and the costly, risky endeavor of building in-house technology. Instead, Olo champions flexibility in service options, seamless ordering and payment, and the adoption of enterprise-grade SaaS platforms that offer greater innovation at a fraction of the cost. This strategic alignment with modern restaurant needs positions Olo as a crucial partner for brands looking to adapt and thrive.

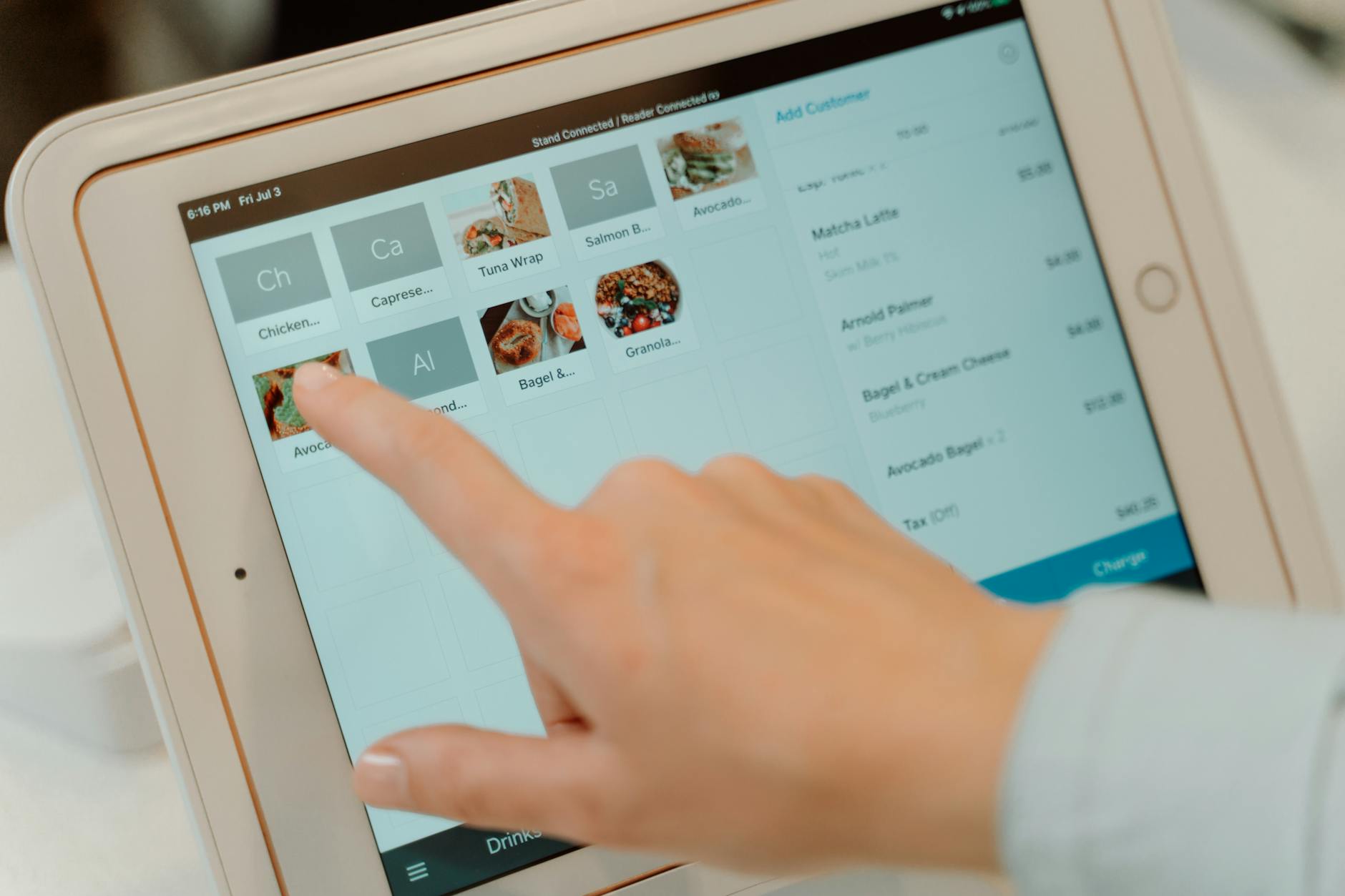

Olo’s comprehensive platform covers digital ordering and delivery through online and mobile modules, ensuring real-time processing and reducing the likelihood of lost orders. This streamlined approach allows restaurant staff to provide accurate wait times and enhance overall satisfaction. By consolidating various operational components into a single unified system, Olo helps restaurants achieve both back-end efficiency and front-end satisfaction, making it a crucial driver of change in an increasingly digital dining landscape.

The company's vision for the future emphasizes leveraging technology to act small even as brands grow, replicating the "Cheers effect" where every guest feels like a known regular. This is achieved by using technology as a foundation to personalize digital orders and free up staff for genuine human connections. Ultimately, Olo aims to redefine dining by optimizing operations and enhancing guest engagement, propelling the industry forward with precision and purpose.

How Does Olo's "Guest Data Flywheel" Drive Value for Restaurants?

At the heart of Olo's strategy is its proprietary "Guest Data Flywheel," a mechanism designed to capture, enrich, and leverage first-party guest data to drive retention and smarter business decisions. This system empowers restaurants to own their guest relationships by facilitating direct ordering through their websites and apps. By collecting structured data from every transaction—including order history, preferences, and behavior—Olo enables restaurants to identify guests, understand their habits, and personalize interactions in real-time, moving beyond the limitations of human memory to deliver "hospitality at scale."

The Guest Data Flywheel integrates Olo's core product suites: Order, Pay, and Engage. The Order module streamlines digital ordering across various channels, while Olo Pay facilitates seamless, insightful payments. This payment stack supports mobile wallets, offers high authorization rates and fraud prevention, and fully integrates with the guest data platform. By consolidating transaction data from online, in-store, catering, and kiosk channels into a single platform, restaurants gain a comprehensive view of guest behavior and preferences, enabling them to track performance metrics, sales trends, and revenue across their business.

AI is a game-changer within this framework, enhancing both operational efficiency and guest experience without replacing human interaction. On the operational side, AI helps restaurants predict kitchen capacity, manage order flow during peak times, and improve wait time accuracy. For customers, AI enables more personalized interactions, from tailored recommendations to seamless ordering and payment experiences. Olo CEO Noah Glass emphasizes that the goal is to remove friction and help humans "do the human things better," ensuring every guest feels like a regular.

This data-driven approach allows restaurants to tailor experiences to individual customers, remembering past orders and greeting them by name. As consumers increasingly prioritize convenience and quick service, the ability to deliver customized experiences through technology becomes a significant competitive advantage. Olo’s platform helps restaurants manage costs more effectively by automating tasks like supply restocks, thereby reducing reliance on labor-intensive solutions amidst rising labor costs and inflation.

What is Olo's Market Position and Growth Trajectory?

Olo has carved out a substantial market position within the restaurant technology sector, particularly in digital ordering and delivery management. As of Q1 2025, Olo served approximately 88,000 active restaurant locations, marking an 8% year-over-year increase. This extensive network underscores its significant presence, processing an average of 2.5 million orders daily in 2024. The company's annual gross merchandise volume (GMV) reached an impressive $29 billion, with gross payment volume (GPV) around $2.8 billion, positioning Olo as the second-largest player in North America by sales volume.

The company's competitive edge is sharpened by its integrated suite of digital ordering solutions and an expansive partner network, boasting over 400 integration partners for broad system compatibility. This allows for a data-driven approach to enhancing guest experience and operational efficiency for restaurant brands. Olo also demonstrates high customer retention rates, with a Net Revenue Retention (NRR) of 111% in Q1 2025, indicating that existing customers are not only staying but also increasing their spending on Olo's services.

Growth opportunities for Olo are substantial, driven by the ongoing digitization of the restaurant industry and the expansion of its product suite. The company is actively expanding its Catering+ module, which offers new revenue streams by addressing the growing demand for digital catering solutions. Furthermore, Olo is enhancing its Olo Pay functionality, aiming to capture more payment volume and deepen customer relationships by integrating transaction data into its Guest Data Flywheel. These strategic expansions are designed to provide more comprehensive solutions and capture a larger share of the market.

Looking ahead, Olo projects full-year 2025 revenue between $338.5 million and $340.0 million. This growth is supported by the company's focus on empowering restaurants to drive profitable customer traffic and streamline operations through its integrated digital platform. The continued growth in digital ordering, coupled with the strategic expansion of services like Catering+, positions Olo to leverage guest data for improved experiences and sustained profitable traffic.

What Are the Key Challenges and Competitive Pressures Facing Olo?

Despite its strong market position, Olo operates within a dynamic and intensely competitive restaurant technology market, facing significant challenges from both direct rivals and indirect forces. Direct competitors include established players like Toast, which reported revenues of $1.06 billion in Q1 2024, offering an all-in-one restaurant management platform. Other direct rivals such as Square, ChowNow, Revel Systems, Deliverect, Tillster, and Zenput also vie for market share with various digital ordering and restaurant management tools. This crowded landscape necessitates continuous innovation and competitive pricing from Olo to maintain its edge.

Indirect competition poses another substantial hurdle, primarily from major third-party delivery marketplaces like DoorDash, Uber Eats, and Grubhub. While Olo often integrates with these platforms for delivery dispatch, they also serve as alternative ordering channels, potentially bypassing Olo's direct ordering solutions. The complex relationship with these aggregators is highlighted by Olo's expanded partnership with Grubhub in February 2025, underscoring the need to collaborate while also competing for customer acquisition.

A significant challenge for Olo has been the departure of marquee enterprise clients, notably Subway in August 2022 and Wingstop in November 2023. These losses raise questions about the stickiness of Olo's core Ordering business, which some critics argue has become commoditized. Furthermore, some large restaurant chains, like Subway and Wingstop, have opted to develop their own proprietary digital ordering and delivery platforms, representing a loss of potential business for Olo and demonstrating the high investment some brands are willing to make for greater control over customer experience and data.

Moreover, Olo faces scrutiny regarding its growth projections and financial reporting. Critics argue that the company's claims of potential revenue growth from "4x more locations" and "6.25x more orders per location" are overly optimistic, if not misleading. Concerns have also been raised about Olo commingling gross payments revenues with SaaS revenues, terming the union "Platform revenues," which allegedly inflates growth rates, Average Revenue Per User (ARPU), and Net Revenue Retention (NRR), thereby obscuring the true performance of its core SaaS business and minimizing cost mismanagement.

How Does Olo's Financial Health and Valuation Stack Up?

Olo's financial health presents a mixed picture, reflecting both growth and underlying profitability challenges. For the trailing twelve months (TTM), the company reported a market capitalization of $1.74 billion and an Enterprise Value (EV) of $1.44 billion. While revenue growth has been robust, with a 24.8% year-over-year increase in FY2024, profitability remains a concern. The TTM net margin stands at -0.3%, with an operating margin of -5.8%, indicating that Olo is not yet consistently profitable. The P/E ratio is negative at -1946.73, reflecting its current unprofitability.

Despite the negative net income, Olo demonstrates strong efficiency in certain areas. Its gross margin is a healthy 53.3%, typical for a SaaS business, suggesting solid unit economics before operating expenses. The company's cash flow generation has shown significant improvement, with operating cash flow growing by 704.3% and free cash flow (FCF) by 297.3% in FY2024. This FCF of $0.22 per share, yielding a TTM P/FCF of 46.95, indicates that Olo is generating cash, which is crucial for future investments and sustaining operations.

From a balance sheet perspective, Olo appears financially sound with a current ratio of 7.72 and a low debt-to-equity ratio of 0.02, suggesting ample liquidity and minimal leverage. However, the company's return on equity (ROE) and return on assets (ROA) are both negative at -0.1%, aligning with its unprofitability. On the other hand, a return on invested capital (ROIC) of 19.1% suggests that the capital deployed is generating a reasonable return, which is a positive sign for long-term value creation.

Analyst sentiment for OLO is currently cautious, with a consensus "Hold" rating from 8 analysts. The median price target is $9.00, which is below the current price of $10.26. Recent rating changes, such as RBC Capital downgrading Olo from Outperform to Sector Perform in July 2025, reflect this tempered outlook. While forward estimates project revenue of $0.4 billion for FY2026 and $0.5 billion for FY2027, along with positive EPS estimates of $0.36 and $0.53 respectively, these are based on a limited number of analysts and come amidst ongoing questions about the company's growth vectors and financial transparency.

What Does Olo's Transition to Private Ownership Mean for Investors?

Olo's strategic decision to partner with Thoma Bravo and transition from public to private ownership in September 2025 marks a pivotal moment for the company. This move, announced live at Thoma Bravo’s 2025 AI Summit, is intended to free Olo from the short-term pressures of public markets, allowing it to move faster, pursue strategic mergers and acquisitions, and invest more aggressively in product innovation, particularly in AI and data-driven solutions. For investors, this means Olo will no longer be trading on the NYSE, and its shares at $10.26 will be acquired as part of the deal.

The take-private deal suggests that Thoma Bravo sees significant untapped potential in Olo's platform and its ability to capitalize on the ongoing digital transformation of the restaurant industry. This private equity backing provides Olo with the capital and strategic guidance to double down on its "hospitality at scale" vision, leveraging AI to enhance both operational efficiency and personalized guest experiences. It also allows Olo to address criticisms regarding its growth and profitability away from quarterly earnings scrutiny.

From an investor perspective, the acquisition by Thoma Bravo provides a clear exit point, albeit at a price that may be below some analysts' long-term projections. The consensus analyst price target of $9.00 was already below the current trading price, suggesting that the market had already factored in some of the challenges Olo faced as a public company. The move to private ownership could ultimately strengthen Olo's market position and accelerate its product roadmap, potentially leading to a more robust company if it were to re-enter public markets in the future.

This transition underscores a broader trend in the tech sector where private equity firms are increasingly acquiring public companies to facilitate long-term strategic overhauls without the immediate demands of public shareholders. For Olo, this means a renewed focus on its core mission, deeper investment in its Guest Data Flywheel, and the flexibility to navigate competitive pressures and market shifts with greater agility.

Olo's journey from a text-message ordering startup to a key player in restaurant tech has been dynamic, culminating in a strategic pivot to private ownership. This move, backed by Thoma Bravo, promises accelerated innovation and strategic growth, free from public market pressures. While current investors will exit, the long-term implications for Olo's role in shaping the future of dining technology remain compelling.

Want deeper research on any stock? Try Kavout Pro for AI-powered analysis, smart signals, and more. Already a member? Add credits to run more research.