Stock News•1 week ago

Will Warsh Cut Rates After a Huge Job Miss?

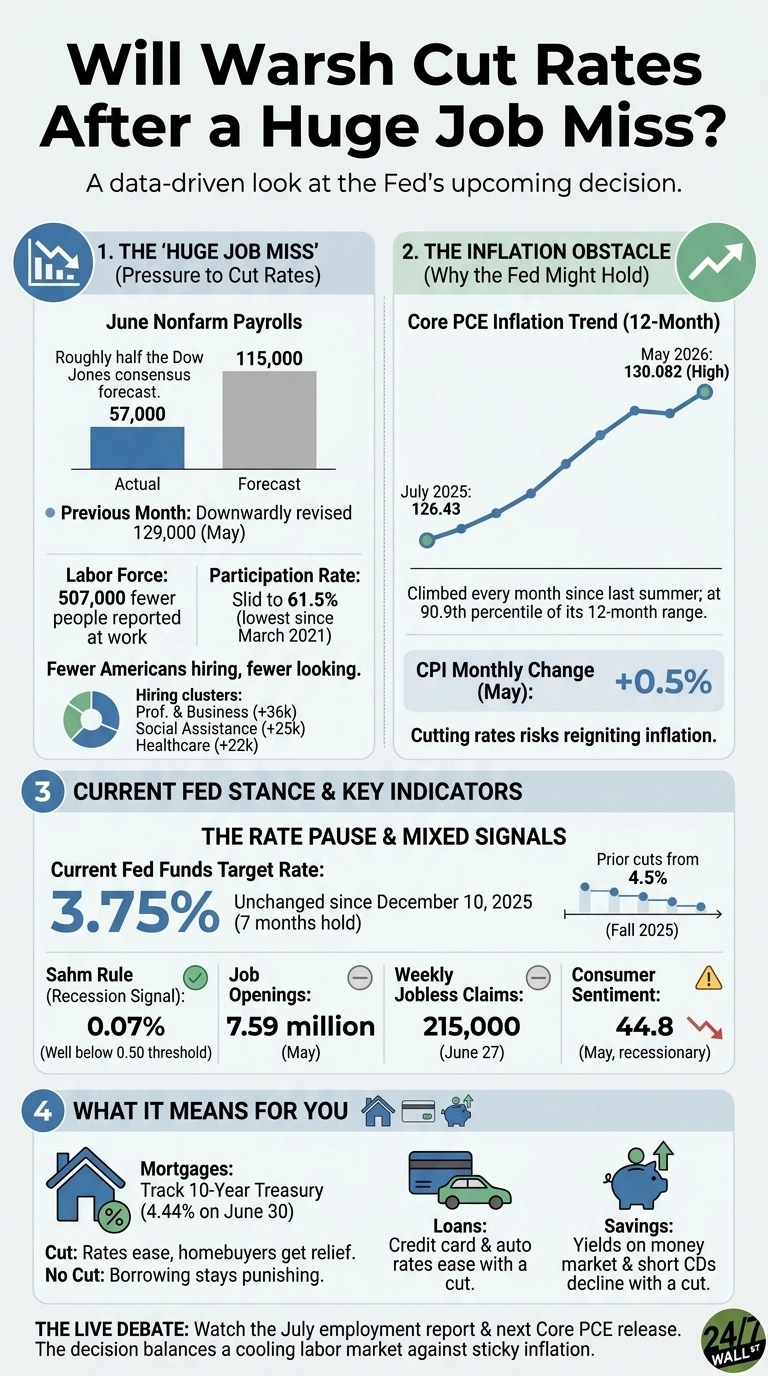

US nonfarm payrolls rose just 57,000 in June, half the 115,000 consensus and down from a revised 129,000 in May, after a sharp labor market cooldown.

Key Takeaways

The latest ADP National Employment Report for March 2026 reveals a U.S. private sector adding a mere 62,000 jobs, marking the slowest pace of hiring since the initial recovery phase of the pandemic. This figure, while a slight dip from February's 63,000 (itself a revision from an initial 22,000), underscores a persistent and material slowdown in the labor market. For context, the economy averaged over 190,000 jobs per month between 2015 and 2019, making the current numbers look anemic by comparison.

This deceleration isn't a sudden shock but rather the continuation of a trend observed throughout 2025. Last year, the U.S. economy added a net total of just 116,000 jobs, representing the weakest annual job growth outside of a recession since 2003. This stark contrast with the robust job growth seen in the preceding years, especially the "Great Reshuffle" period of 2022 where an average of 6.4 million workers were hired monthly, highlights a significant shift in hiring dynamics.

The apparent disconnect between resilient economic growth—real GDP grew 2.0% in 2025—and the sharp slowdown in hiring has been a puzzling feature of the current cycle. While the unemployment rate has remained historically low, hovering around 4.40% as of February 2026, this stability may mask underlying weaknesses. The Federal Reserve has been closely watching these indicators, with Chair Jerome Powell previously suggesting that payroll growth might even have been negative by 20,000 jobs on a monthly basis since April 2025.

This "slow-hire, slow-fire" dynamic, where businesses are hesitant to expand but also reluctant to lay off existing staff, defines the current environment. It suggests a cautious approach from employers facing a landscape of economic uncertainty, from fluctuating input costs to geopolitical tensions. The March figures confirm that this cautious stance is hardening, pushing the labor market further into a territory not seen since the immediate aftermath of the pandemic's initial shock.

The headline job numbers only tell part of the story; a deeper dive reveals a highly concentrated and increasingly fragile labor market. The vast majority of job growth in 2025 was a one-sector phenomenon, almost entirely driven by health care and social assistance, which added a staggering 686,100 jobs. In sharp contrast, all other industry groups combined declined by over 500,000 jobs, with significant losses in government employment, manufacturing, trade, transportation, information services, and professional services.

This lack of breadth in hiring is a critical warning sign. While health services continue to be a long-standing source of employment growth, the sustained weakness across other sectors indicates a broader economic malaise. For instance, February's 63,000 private job additions were primarily concentrated in health services and construction, with other sectors either flat or declining. This narrow base of growth makes the overall labor market vulnerable to shifts in these few dominant industries.

A significant contributing factor to this slowdown is the evolving landscape of immigration. Tighter immigration policies and falling fertility rates are poised to weigh heavily on labor supply. Net international migration into the United States is projected to fall dramatically, from 2.7 million in the year ending July 1, 2024, to an estimated 321,000 by July 1, 2026. This decline in new workers, coupled with an aging population and fewer visa issuances, directly impacts the available labor pool, particularly in sectors that traditionally employ large shares of immigrants like construction, transportation, and manufacturing—precisely the sectors seeing sharper slowdowns in hiring.

Furthermore, economic uncertainty continues to loom large. The introduction of reciprocal tariffs in early April 2025 created significant uncertainty around input costs, leading many businesses to pause or delay hiring plans. This was exacerbated by a government shutdown in October 2025, which resulted in a large loss of jobs. More recently, rising geopolitical tensions in the Middle East have increased commodity prices, including oil and gas, adding another layer of cost pressure and uncertainty that could further deter hiring managers from expansion.

Despite the significant slowdown in job creation, wage growth remains stubbornly elevated, presenting a complex challenge for the Federal Reserve. For those staying in their jobs, annual pay grew by a solid 4.5% in February, while wage gains for job switchers, though moderating, still stood at 6.3%. This 1.8% gap between job-stayers and job-switchers is the smallest since ADP began tracking the metric, suggesting that while the premium for switching jobs has decreased, overall wage pressures persist.

This elevated wage growth, particularly for job-stayers, continues to fuel concerns about inflation. The Fed's primary mandate is price stability, and strong wage gains can translate into higher consumer spending and upward pressure on prices, making the fight against inflation more difficult. Even with the labor market cooling on the hiring front, the underlying strength in wages indicates that inflationary impulses are still present within the economy.

The Fed has already responded to the mixed signals, cutting its key lending rate three times in 2025, starting in September, bringing it to around 3.6%—the lowest level in three years. However, policymakers remain divided on how much further borrowing costs should go. The current U.S. Treasury yield curve reflects this uncertainty, with the 10-year yield at 4.30% and the 2s/10s spread at a positive +0.51%, indicating a normalized, but still elevated, interest rate environment. The upcoming FOMC Minutes on April 8, 2026, will be closely scrutinized for further clues on the Fed's thinking regarding future rate actions.

The Bank of America's internal data also highlights a concerning disparity in wage growth. In January 2026, higher-income households saw after-tax wage and salary growth of 3.7% year-over-year, while lower-income households experienced a much weaker 0.9% growth. This divergence suggests that while aggregate wage data might appear strong, the benefits are not evenly distributed, potentially exacerbating economic inequality and creating different spending patterns across income brackets. This unevenness adds another layer of complexity to the Fed's assessment of the overall economic health and inflationary pressures.

The confluence of slowing job growth, concentrated hiring, persistent wage pressures, and external uncertainties paints a nuanced picture for the U.S. economy in 2026. The "decoupling" of GDP growth from job creation, as some analysts suggest, implies that the economy is expanding without generating a commensurate number of new roles. This could be driven by factors like improved productivity, particularly from new technologies like artificial intelligence, or simply a more efficient use of existing labor. However, it also means that the benefits of economic growth might not be broadly distributed through widespread employment opportunities.

The slowdown in hiring is not just about numbers; it reflects a shift in worker confidence and behavior. The quits rate, which measures how many people are voluntarily leaving their jobs, is now lower than pre-COVID levels. This indicates decreased confidence among workers in finding new roles, leading them to hold onto their current positions. This lack of turnover, in turn, means fewer job openings for new entrants or those seeking career advancement, creating a bottleneck in the labor market. The Federal Reserve Bank of New York's survey in December 2025 found workers more worried about job security and less confident about finding new employment if laid off.

Looking ahead, the first half of 2026 is likely to deliver uncomfortably slow growth in the labor market, with unemployment potentially peaking at 4.5% in early 2026. The sustainable pace of monthly job growth is estimated to be between 20,000 and 50,000 at the end of 2025, suggesting that the current March figure of 62,000 is still marginally above this "stable" range, but barely. This delicate balance means that any significant negative shock could easily push job creation into contraction territory.

The ongoing geopolitical tensions, particularly in the Middle East, represent a critical wildcard. A prolonged period of elevated tensions and increased commodity prices could further dampen business confidence and hiring plans. Rising non-labor input costs might force companies to consider reductions in labor costs, potentially extending or worsening the current hiring slump. This new layer of economic uncertainty adds to the existing challenges, making the outlook for both the consumer and the broader economy increasingly precarious.

For investors, the current labor market dynamics present a complex environment that demands careful consideration. The slowing job growth, while potentially easing some inflationary pressures in the long run, also signals a deceleration in economic momentum. This could translate into lower corporate earnings growth, particularly for consumer-facing sectors that rely on robust employment and wage gains to drive demand. Investors should scrutinize company guidance for any signs of hiring freezes or cost-cutting measures.

The Federal Reserve's path forward remains highly data-dependent. While the slowdown in hiring might suggest a greater likelihood of future rate cuts, the persistent wage inflation could temper the Fed's dovishness. The market will be closely watching upcoming economic data, especially inflation reports and further employment figures, for clearer signals. A "higher for longer" interest rate scenario remains a distinct possibility if inflation proves stickier than expected, which could continue to pressure growth stocks and favor value-oriented investments.

Furthermore, the sectoral concentration of job growth highlights areas of resilience and vulnerability. Industries like healthcare and social assistance may offer more stable investment opportunities due to their consistent demand, while sectors experiencing declines, such as manufacturing and professional services, could face headwinds. Investors should consider diversifying their portfolios to mitigate risks associated with a narrowly driven labor market and be prepared for continued volatility as the economy navigates these uncertain waters.

The U.S. labor market is undoubtedly at a crossroads, moving from a period of post-pandemic exuberance to one of cautious recalibration. The March job report reinforces the narrative of a cooling economy, but one still grappling with inflationary undercurrents. Investors must remain agile, focusing on companies with strong fundamentals, pricing power, and resilience against both economic slowdowns and persistent cost pressures.

Want deeper research on any stock? Try Kavout Pro for AI-powered analysis, smart signals, and more. Already a member? Add credits to run more research.