Crypto News•5 days ago

$1.5 Billion Worth of ETH and BTC Options on Track to Expire

~$1.45B in Bitcoin and Ethereum options expire on Deribit, potentially increasing near-term volatility as traders roll or close positions.

Key Takeaways

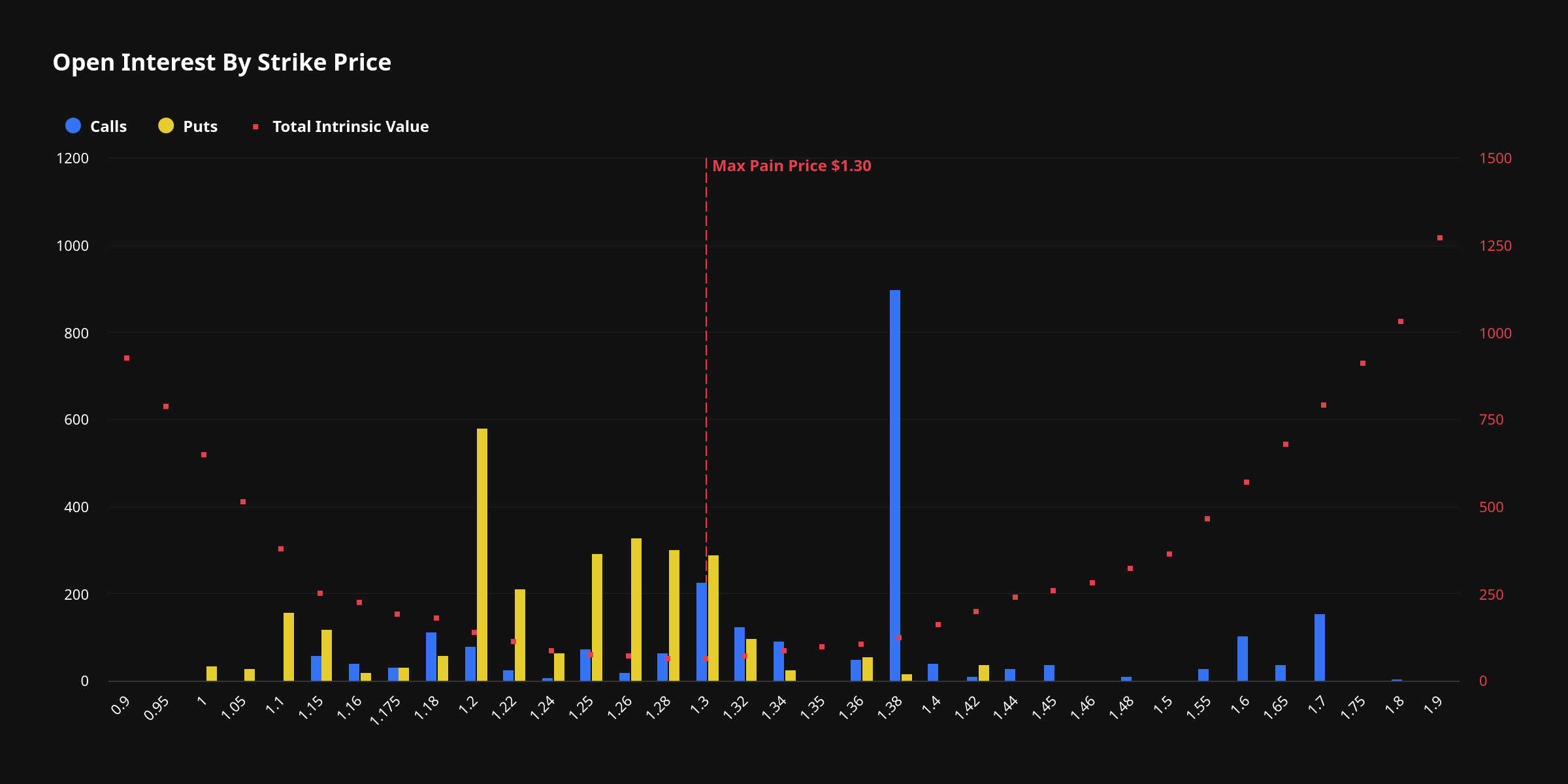

Coinbase Global (NASDAQ: COIN) is currently navigating a turbulent market, evidenced by a flurry of unusual options activity that points to a decidedly bearish sentiment among some institutional players. On February 26, Benzinga's options scanner flagged 85 extraordinary options activities for Coinbase, with a clear lean towards puts. While 34% of these deep-pocketed investors were bullish, a significant 55% adopted a bearish stance, highlighting a palpable unease about the crypto exchange's near-term prospects.

This bearish tilt isn't just theoretical; it's backed by substantial capital. A particularly striking trade on February 19 involved a put option with a $200.00 strike price expiring on February 20, 2026. This single trade saw 21,550 contracts change hands, generating an $80.92 million turnover and a premium of $37.9 million. Such a large, out-of-the-money put indicates a strong conviction that Coinbase's stock could fall significantly below its current trading price of $175.85 by the expiration date.

The market's apprehension isn't without reason. COIN has been on a downward trajectory, shedding 26% year-to-date. Over the past month, shares have crashed 32%, extending to a 37% decline over three months and 38% over the last 52-week period. This performance starkly contrasts with its 52-week high of $444.65, with the stock now trading 63% below that peak. The underlying cause is a broader crypto market pullback, with Bitcoin falling 24% year-to-date and 30% over the past month, from its October high of $126,000 to around $66,500.

This significant put activity, especially the large February 2026 contract, suggests that some sophisticated investors are betting on continued weakness, potentially anticipating further declines in crypto asset prices or a deterioration in Coinbase's core business. It's a stark warning that despite the long-term bullish outlook from some analysts, the immediate future for Coinbase could be fraught with challenges. The sheer scale of these bearish bets cannot be ignored by retail investors trying to gauge the true sentiment surrounding COIN.

In response to the severe liquidity freeze and collapsing trading volumes in the crypto market, Coinbase has embarked on an ambitious "Everything Exchange" strategy, expanding into traditional stock trading. The company recently rolled out 24/5 commission-free trading on over 8,000 U.S.-listed stocks and ETFs to all U.S. users. This move is a direct assault on the retail brokerage market, aiming to diversify revenue streams and reduce its heavy reliance on volatile crypto transaction fees.

A key differentiator in this new offering is the ability for users to fund trades directly with U.S. dollars or USDC, Coinbase's own stablecoin. This seamless integration leverages the existing $100+ billion in USDC supply on Coinbase's platform, potentially converting idle stablecoin balances into equity trading volume. If even a fraction of this capital flows into equities, it could provide a much-needed liquidity lifeline, offsetting the sharp decline in crypto trading activity. Coinbase's own trading volume dropped 40% year-over-year in Q4 2025 to $264 billion, with January activity trending even lower.

The strategic intent is clear: CEO Brian Armstrong aims to loosen the tie between COIN's share price and Bitcoin's volatility. By becoming a comprehensive financial super app, Coinbase hopes to build a more durable earnings base. This pivot is critical, especially after a mixed Q4 2025 earnings report where revenue fell 5% quarter-over-quarter to $1.7 billion, and transaction revenue plummeted 6% to $983 million. Despite these headwinds, Coinbase did achieve its 12th consecutive quarter of adjusted EBITDA profitability, a testament to its operational resilience.

However, this aggressive expansion into a crowded retail brokerage market, dominated by established players like Robinhood and SoFi, comes with significant risks. Coinbase risks diluting its unique brand identity as a crypto-native platform, potentially becoming just another generic trading app. More importantly, venturing into broader securities activities introduces a new layer of compliance complexity and regulatory oversight that the company is not currently structured for. The muted market reaction to this strategy suggests investors are still weighing whether this diversification is a genuine lifeline or a costly distraction.

The divergence in sentiment between Wall Street analysts and retail investors regarding Coinbase is striking, creating a complex picture for potential investors. Despite the stock's significant decline and the recent bearish options activity, Wall Street maintains a largely optimistic outlook. The consensus analyst rating for COIN is a "Buy," with 20 out of 35 analysts issuing a "Buy" recommendation, 12 a "Hold," and only 3 a "Sell." The average price target stands at $274.56, with a median of $272.00, implying substantial upside from the current $175.85 price.

This bullish analyst stance is largely predicated on Coinbase's "Everything Exchange" vision and its efforts to diversify revenue beyond volatile crypto trading. Analysts are giving credit for the company's pivot, seeing it as a move towards becoming a diversified fintech platform rather than just a crypto trading desk. For example, Goldman Sachs maintained a "Buy" rating on February 17, while Cantor Fitzgerald kept an "Overweight" rating with a target price of $221. This institutional optimism suggests a belief in Coinbase's long-term strategic direction and its ability to adapt to market changes.

However, retail sentiment, particularly on platforms like Reddit's r/wallstreetbets, tells a much harsher story. The community remains deeply bearish, with Coinbase's social sentiment score hitting a 48-hour low of 18 out of 100 recently. Retail traders are focused on Coinbase's vulnerability to crypto trading volumes drying up, with posts like "Yeah I'm cooked" capturing the widespread pain and skepticism. This stark contrast highlights a fundamental disagreement: institutional analysts are betting on strategic diversification, while retail investors are fixated on the immediate impact of crypto market downturns on Coinbase's core business.

The recent Q4 2025 earnings report, which saw Coinbase post a $667 million net loss—its first profit miss since Q3 2023—further fueled retail skepticism. While the stock initially jumped 16% post-earnings, suggesting some investors were pricing in the diversification story, the subsequent decline and bearish options activity indicate that the market remains highly sensitive to actual financial performance. The gap between analyst price targets and retail sentiment is a critical watchpoint, as it often signals underlying market tensions and differing interpretations of a company's future trajectory.

Coinbase's financial performance is a complex interplay of significant headwinds and potential tailwinds, making its future trajectory highly uncertain. The most immediate headwind is the severe contraction in crypto trading volumes. Total spot trading volume on centralized crypto exchanges fell to $1.13 trillion in December, a 32% drop from November and a 49% decline from October, marking the lowest monthly level since September 2024. This directly impacts Coinbase's transaction revenue, which plummeted 37% to $982.7 million in Q4 2025, missing analyst expectations.

Adding to the pressure, Coinbase reported a $667 million net loss in Q4 2025, its first profit miss in eight quarters. A significant portion of this loss stemmed from unrealized losses on its own crypto holdings as prices collapsed. Furthermore, Q1 2026 subscription revenue guidance was lowered to $550 million-$630 million, down from $727 million in Q4. This signals that even the company's more stable revenue streams are feeling the pinch, making the path to sustained profitability more challenging. The heavy reliance on retail revenue and increasing industry competition also remain persistent bear case arguments.

However, several tailwinds could provide a much-needed boost. Coinbase's diversification into stock trading, leveraging its USDC stablecoin, aims to create a new, less volatile revenue stream. The company's institutional strategy also remains robust; Coinbase's Head of Institutional Strategy, John D’Agostino, noted that institutional investors surveyed in Hong Kong and the UAE have not changed their long-term thesis on Bitcoin as a store of value, with "net buying exceeding net selling" on the platform. This consistent institutional interest could provide a floor for demand.

Regulatory clarity, such as the passage of the GENIUS Act for stablecoins, could also act as a tailwind by legitimizing operations and encouraging broader institutional participation. Coinbase's continued focus on its "everything exchange" vision, expanding into derivatives, tokenized equities, and prediction markets, aims to capture value across the entire crypto ecosystem. While these initiatives have yet to materially impact revenue, they reflect a strategic push towards a more durable earnings base, with subscription and services now accounting for 41% of net revenue, up from 39% in Q3 2025.

For investors eyeing Coinbase (COIN), the current landscape presents a high-stakes dilemma, balancing significant short-term risks with long-term strategic potential. The substantial bearish options activity, particularly the $37.9 million put trade, serves as a potent warning that sophisticated investors are bracing for further downside. This sentiment is reinforced by COIN's 26% year-to-date decline and the broader crypto market's volatility, which directly impacts Coinbase's core transaction revenue.

However, it's crucial not to overlook the underlying strengths and strategic pivots. Coinbase's "Buy" consensus rating from Wall Street analysts, with an average price target implying significant upside, suggests a belief in the company's long-term vision. The "Everything Exchange" strategy, aiming to diversify into commission-free stock trading and leverage its USDC ecosystem, is a bold move to stabilize revenue and decouple its performance from pure crypto volatility. If successful, this could transform Coinbase into a broader fintech powerhouse, justifying higher valuations.

Investors should closely monitor several key metrics. First, track Coinbase's total daily trading volume, now encompassing both crypto and stocks, to gauge the success of its diversification efforts. A sustained increase would indicate real traction. Second, observe changes in COIN's correlation to Bitcoin; a successful "Everything Exchange" strategy should see COIN's price action become less tethered to BTC's swings. Finally, keep an eye on subscription and services revenue, especially given the lowered Q1 2026 guidance, as this segment is critical for building a more resilient earnings base.

Ultimately, investing in Coinbase right now is a bet on its ability to execute its ambitious diversification strategy amidst a challenging regulatory and market environment. The current bearish options activity signals immediate concerns, but the analyst community sees a path to significant long-term growth. This is not an investment for the faint of heart, demanding a deep understanding of both the crypto market's inherent volatility and Coinbase's strategic evolution.

Coinbase remains a high-conviction play for those believing in the long-term convergence of traditional finance and crypto, but the current bearish options activity highlights significant near-term headwinds. Investors should exercise caution, closely monitoring the success of its diversification efforts and the broader crypto market's trajectory. The path ahead for COIN is likely to be volatile, but its strategic pivots could unlock substantial value if executed effectively.

Want deeper research on any stock? Try Kavout Pro for AI-powered analysis, smart signals, and more. Already a member? Add credits to run more research.