Stock News•2 days ago

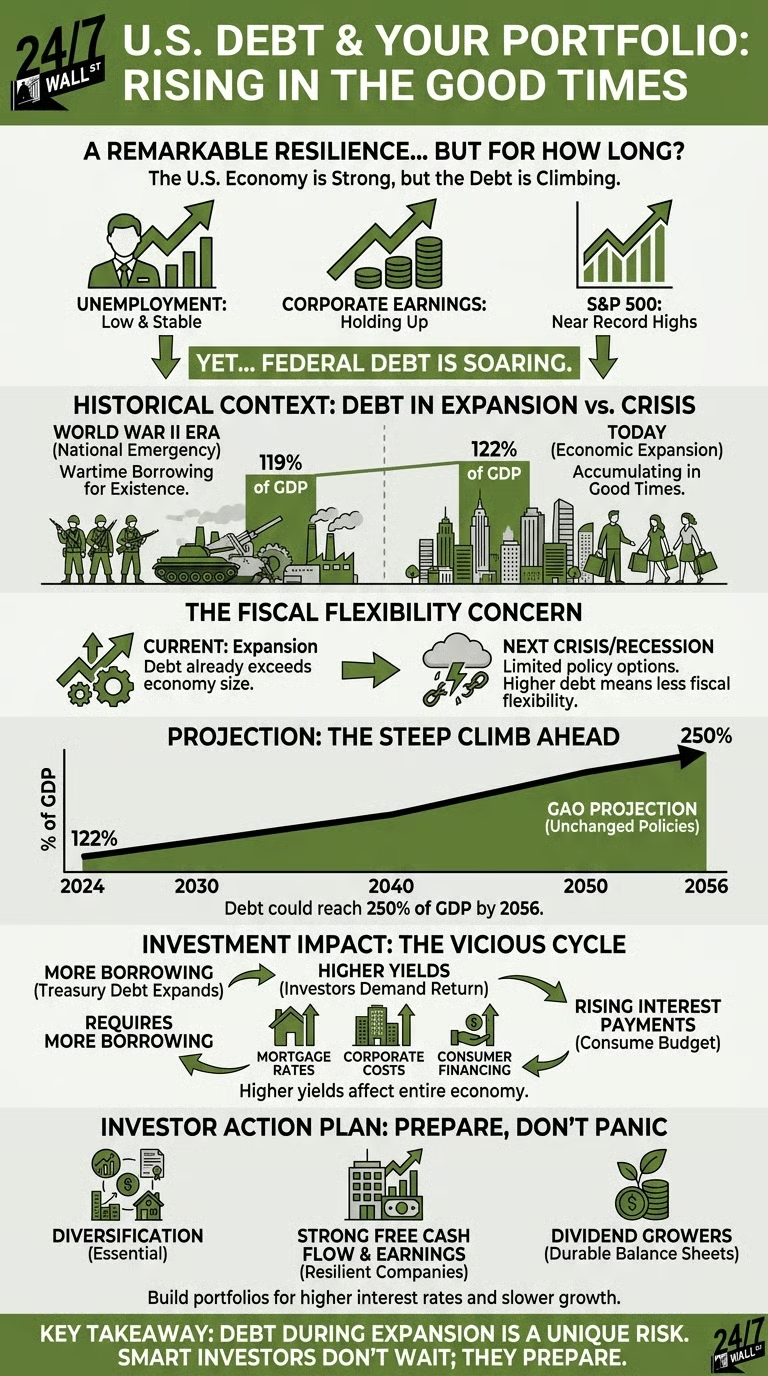

U.S. Debt Smashes WWII Record — But It’s About to Get So Much Worse

U.S. federal debt surpassed its WWII-era record as a share of GDP, with the trajectory worsening before the next recession, potentially pressuring portfolios.

Key Takeaways

Nouriel Roubini, the economist famously dubbed "Dr. Doom" for his prescient warnings ahead of the 2008 financial crisis, is now presenting a surprisingly nuanced, even moderately optimistic, outlook for the US economy. While geopolitical tensions, particularly the ongoing US war on Iran, continue to cast a shadow, Roubini argues that the transformative power of artificial intelligence (AI) is poised to anchor a new era of American exceptionalism. This shift from his historically bearish stance suggests a complex interplay of risks and opportunities that investors must carefully navigate.

Roubini, a professor emeritus at NYU Stern and CEO of Roubini Macro Associates, believes that the gains from AI could outweigh the combined drag of tariffs, fiscal risks, and geopolitical shocks by a significant four-to-one ratio. He posits that technology is "first order," while everything else, including geopolitics, is "second order." This perspective challenges conventional wisdom that often prioritizes immediate geopolitical disruptions over long-term technological shifts.

His analysis, shared in recent interviews and op-eds, forecasts US economic growth could reach as high as 4% by the end of the decade, a substantial increase from the current estimated potential growth of 1.8%. This acceleration is largely attributed to AI-driven productivity gains, which he expects to drive around half of that potential growth. Such a robust long-term outlook provides a compelling counter-narrative to the prevailing anxieties surrounding global conflicts and inflationary pressures.

Despite this long-term optimism, Roubini acknowledges immediate headwinds. He previously warned of a shallow US recession by late 2025 due to tariffs, a forecast that has since evolved. The current situation, marked by the Iran war, introduces new inflationary pressures, but he maintains that a full-blown recession is not the most likely outcome, provided the conflict remains contained and oil prices do not skyrocket indefinitely.

The US war on Iran is undeniably creating significant economic ripples, primarily through its impact on energy markets and consumer sentiment. While the stock market has shown remarkable resilience, the conflict has pushed oil prices well above $100 per barrel, raising concerns about a sustained inflationary environment and its potential to derail economic growth. This surge in energy costs directly affects household budgets and business operations.

Nouriel Roubini characterizes the economic hit from the Iran war as "moderate" for the US, provided the conflict is relatively short-lived. He notes that if oil prices remain above $100 per barrel until the end of April, the impact on inflation and growth will be greater, but still "not enough to put the economy into a recession." This assessment hinges on the market's current expectation that the war will not last much longer, a sentiment that could shift rapidly with any escalation.

However, cracks are beginning to emerge. The University of Michigan’s preliminary consumer sentiment reading for March plummeted to 55.5, its lowest level of 2026. This sharp decline completely erased earlier gains in consumer optimism, with expectations for personal finances falling 7.5% nationally across all income levels. Such a drop in confidence signals that households are feeling the pinch of higher prices and increased uncertainty.

Furthermore, flash PMI manufacturing surveys for March indicate a sharp slowdown in activity, suggesting that businesses are also reacting to the volatile environment. Historically, significant spikes in oil prices have often preceded global recessions, as seen in the 1973, 1978, and 2008 crises. While Roubini doesn't foresee a repeat of the 1970s stagflation, the risk of a "growth recession"—below-trend GDP growth—remains a tangible threat, particularly if the Federal Reserve is forced to delay rate cuts to combat persistent inflation.

The ongoing war in Iran and its inflationary implications have placed the Federal Reserve in a precarious position, forcing a re-evaluation of its monetary policy trajectory. With the current inflation rate at 2.34% and the Federal Funds Rate at 3.64%, the Fed's primary objective of bringing inflation down to its 2% target while maintaining economic stability faces significant headwinds. The market's expectation for rate cuts is now being delayed, with limited easing anticipated in 2026.

Roubini highlights the critical distinction between temporary price level increases and a sustained rise in inflation expectations. If inflation expectations become "de-anchored" due to prolonged high oil prices, the Fed would be compelled to raise policy rates, risking a deeper economic slowdown. This scenario is a central banker's nightmare, as it could lead to a permanent increase in inflation, undermining long-term stability.

The current US Treasury yield curve reflects a relatively normal environment, with the 2s/10s spread at +0.46%. However, the persistent inflationary pressures from the Iran conflict could challenge this stability. A prolonged period of high oil prices could force the Fed to remain on hold, adopting a cautious, data-dependent stance, as outlined in a recent paper co-authored by Roubini. This prolonged pause in policy would weigh on sectors sensitive to interest rates, such as housing and corporate borrowing.

Upcoming economic events, including the Gross Domestic Product QoQ (Q4) and Core PCE Price Index MoM (Feb) on April 9, will be closely watched for clues on the economy's health and inflationary trends. A weaker-than-expected GDP growth rate or a higher-than-anticipated PCE reading could further complicate the Fed's decision-making. The FOMC Minutes, scheduled for April 8, will also provide crucial insights into the central bank's internal discussions and future policy leanings amidst the geopolitical uncertainty.

Nouriel Roubini's surprising optimism largely hinges on the transformative potential of artificial intelligence, which he believes will usher in an era of "US exceptionalism" and significantly boost productivity. He argues that AI, robotics, and quantum computing give America a distinct edge, capable of driving yearly growth from 1.8% to as high as 4% by the end of the decade. This isn't just a marginal improvement; it's a fundamental re-rating of the US economy's potential.

This bullish stance on AI is rooted in the belief that artificial general intelligence (AGI) is closer than many realize, potentially just three to five years away. Roubini suggests that companies successfully engineering AGI could scale as much as fivefold in the near term, justifying current high valuations in the tech sector. While he acknowledges that not all "Magnificent Seven" firms will achieve this, he expects three or four to lead the charge, driving massive investment and innovation.

However, the impact of AI on the labor market presents a complex picture. While AI is expected to create new infrastructure and startup jobs in the short term, Roubini also foresees "massive amounts of labor shedding" over the medium to long term. This is already evident in layoffs at major tech firms like Amazon (AMZN) and Meta (META), with a recent survey indicating a 4% net reduction in jobs across sectors most impacted by AI adoption, particularly among early-career employees.

The market's current bet on AI is somewhat incoherent, with both "doom" and "boom" narratives coexisting. While some fear AI-driven economic contraction, others point to the potential for AI to compress service costs by 40-70%, allowing households to afford more even with less income. This "Capability-Dissipation Gap"—the widening distance between what AI can do and what the economy has reorganized around it—suggests that the economic rewards for early adopters will be larger and more persistent than currently priced.

Beyond the immediate concerns of the Iran war, Roubini acknowledges a broader landscape of geopolitical and fiscal risks, though he believes AI's impact will largely offset them. The persistent tensions between the US and China, for instance, remain a significant factor, even as Roubini downplays their market impact, noting that financial markets have largely ignored such risks in recent decades. However, the "Great Economic Rivalry" between the two superpowers continues to shape global trade and technological competition.

President Donald Trump's tariffs and other protectionist policies have been a recurring theme in Roubini's analysis, previously contributing to a "bumpy year" for the US economy in 2025. While the administration has since negotiated more modest tariff increases, the potential for renewed trade wars under future administrations remains a fiscal risk. Roubini estimates that even a 10% universal tariff and a 60% tariff on China would only dent US growth by half a percentage point, a drag he believes is easily overcome by tech advancements.

The global economy's resilience to external shocks is a key tenet of Roubini's current outlook. He points to the brief wobble in oil prices during the Israel-Iran clash in mid-2025, which markets quickly "looked through." This suggests a higher tolerance for geopolitical disruptions than many investors assume, reinforcing his view that "technology trumps tariffs" and other "second order" risks.

However, not all economists share this sanguine view. The IMF, for instance, has warned about "investor exuberance" and "pockets of valuation frothiness" in credit markets, drawing parallels to the late 1990s dot-com boom. JPMorgan CEO Jamie Dimon's caution about "cockroaches" in the credit market underscores the potential for hidden risks to emerge. While Roubini's AI-driven optimism is compelling, investors must remain vigilant about these underlying vulnerabilities and the potential for unforeseen "black swan" events.

Investors face a complex and nuanced landscape, where traditional "Dr. Doom" warnings are tempered by a powerful technological optimism. The immediate challenge lies in the inflationary pressures from the Iran war, which could keep oil prices elevated and delay anticipated Fed rate cuts. This suggests a cautious approach to short-term market movements, with a focus on companies resilient to higher input costs.

However, Roubini's long-term bullishness on AI presents a compelling argument for strategic positioning in the technology sector. Identifying the "three or four" firms within the Magnificent Seven that are truly poised to engineer AGI could yield substantial returns. This requires a deep dive beyond surface-level narratives, focusing on companies with robust R&D, strong intellectual property, and clear pathways to scaling AI solutions.

Diversification remains key. While the US economy is expected to outperform, global growth is slowing, with the Eurozone potentially seeing GDP growth slow to 0.5% and China falling below 3% if the Iran war persists. Investors should consider exposure to defensive assets like gold, which has seen a significant rise to $4,427.60, and maintain a strategic cash position to capitalize on potential market dislocations. The current environment demands a balanced portfolio, blending growth opportunities with defensive safeguards.

Want deeper research on any stock? Try Kavout Pro for AI-powered analysis, smart signals, and more. Already a member? Add credits to run more research.