Key Takeaways

- Lumentum Holdings (LITE) is emerging as a critical enabler of the AI revolution, with its optical and photonic components powering high-speed data transmission in hyperscale data centers.

- The company delivered a blowout Q2 FY26, beating revenue and EPS estimates significantly, and provided robust Q3 guidance, driven by accelerating demand for its Optical Circuit Switches (OCS) and Co-Packaged Optics (CPO).

- Despite a substantial run-up in its stock price, Lumentum's strategic partnerships, technological leadership, and expanding product portfolio position it for continued growth within the multi-year AI infrastructure buildout.

Is Lumentum Holdings (LITE) the AI Infrastructure Play Investors Are Overlooking?

Lumentum Holdings (NASDAQ: LITE) has quietly become a foundational player in the artificial intelligence (AI) revolution, with its stock surging as the market recognizes its pivotal role in the massive data center buildout. Trading at $670.50 as of February 23, 2026, LITE has seen an impressive run, climbing 56% year-to-date in 2026 and a staggering 722.4% over the past 12 months, far outpacing many peers. This performance is directly tied to the unprecedented capital expenditures by hyperscalers, projected to reach $700 billion in 2026, a significant jump from $394 billion in 2025.

The company, with a market capitalization of $47.87 billion, designs and manufactures optical and photonic networking components essential for the high-speed data transmission required by AI workloads. Lumentum's CEO, Michael Hurlston, has emphatically stated that "Virtually every AI network is powered by Lumentum technology," underscoring its embedded position within the AI ecosystem. This isn't just about chips; it's about the intricate optical infrastructure that allows AI processors to communicate at lightning speed, a bottleneck that Lumentum is uniquely positioned to solve.

The recent surge in LITE's stock price reflects growing investor optimism, with the company frequently appearing on analysts' top picks for 2026 in the semiconductor and equipment sectors. This sentiment is fueled by Lumentum's technological edge and its ability to translate that into robust financial performance. The question for many investors now is whether this momentum is sustainable, or if the market has already priced in the company's future growth potential.

Lumentum's journey from a cyclical optical component supplier to a structural AI infrastructure provider marks a significant inflection point. Its products are no longer just enabling general data traffic; they are specifically optimized for the unique demands of AI, from training large language models to inference at the edge. This strategic pivot, combined with strong execution, has put Lumentum on a trajectory that analysts believe could make it one of the best-performing AI-related stocks of the year.

How is Lumentum Capitalizing on the AI Data Center Boom?

Lumentum's impressive financial results for fiscal Q2 2026, ended December 27, 2025, offer a clear window into how effectively the company is capitalizing on the AI data center boom. The company reported revenue of $665.5 million, a substantial 66% year-over-year increase, comfortably beating Wall Street estimates of $652 million. Even more striking, non-GAAP earnings per share (EPS) soared to $1.67, nearly quadrupling from the prior year and crushing the consensus expectation of $1.41. This marks the eighth consecutive quarter Lumentum has surpassed EPS estimates, demonstrating consistent operational excellence.

The growth is not accidental; it's driven by Lumentum's critical role in providing high-speed optical components for next-generation network architectures. The company's Optical Circuit Switches (OCS) and Co-Packaged Optics (CPO) are at the forefront of this demand. Lumentum boasts a robust backlog of over $400 million for its OCS products, with the majority slated for shipment in the second half of calendar year 2026. Furthermore, the company secured a "multi-hundred-million-dollar" contract for CPO, which are vital for their higher bandwidth and energy efficiency in custom AI processors.

Lumentum's collaboration with NVIDIA is another key differentiator, as it actively contributes to developing NVIDIA's silicon photonics ecosystem, particularly for the deployment of Spectrum-X Photonics networking switches. This strategic partnership embeds Lumentum deeper into the AI supply chain, ensuring its technology is integral to leading AI platforms. The company's Components segment, which includes laser chips and assemblies, saw revenue jump 17% quarter-over-quarter and 68% year-over-year to $443.7 million, now representing 66.7% of total revenue.

Management's Q3 FY26 guidance further underscores this accelerating momentum, projecting revenue between $780 million and $830 million, representing an impressive 85%+ year-over-year increase at the midpoint. Non-GAAP EPS is expected to be in the range of $2.15 to $2.35. This strong outlook suggests that Lumentum is not just riding a wave but is actively shaping the future of AI infrastructure with its innovative and high-demand optical solutions.

What Are Lumentum's Key Technological Advantages and Strategic Positioning?

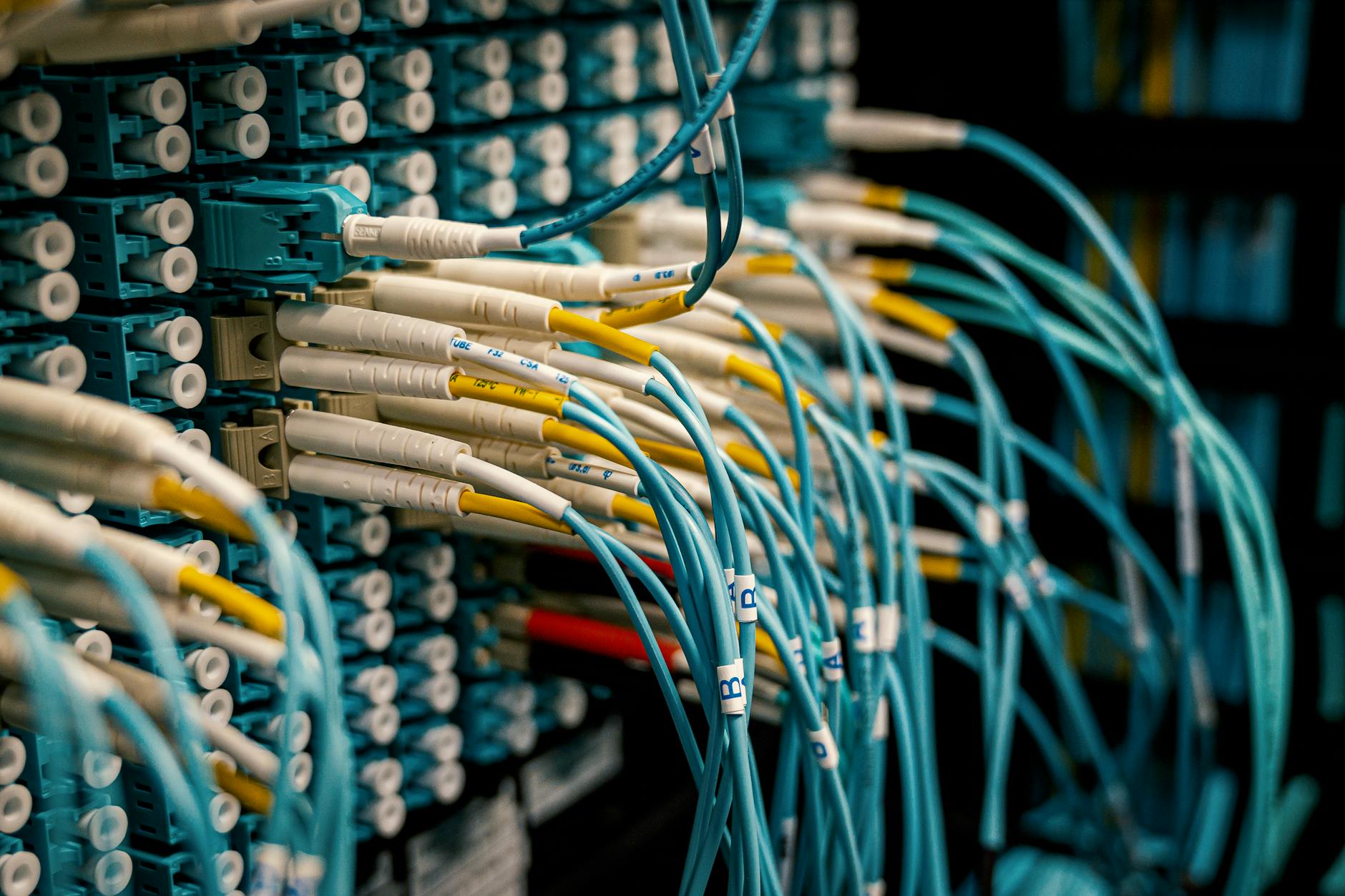

Lumentum's technological advantages lie in its comprehensive portfolio of optical and photonic solutions, which are becoming indispensable for the evolving demands of AI data centers. The company's leadership in high-speed optical components addresses critical challenges like bandwidth saturation and power efficiency in modern AI workloads. Its product suite, including EML laser chips, optical transceivers, Optical Circuit Switches (OCS), and Co-Packaged Optics (CPO), forms the backbone of AI data center infrastructure, enabling seamless, high-speed data movement.

The company has achieved new records in 100G and 200G EML (Electro-absorption Modulated Laser) shipments, with 200G EMLs contributing approximately 10% of its datacom chip revenue. These advanced lasers are crucial for the dense, high-bandwidth interconnects within AI clusters. Moreover, Lumentum has seen its eighth straight sequential quarter of growth in narrow linewidth lasers for Data Center Interconnect (DCI), highlighting its consistent innovation and market penetration in specialized optical technologies.

Lumentum's strategic positioning is further solidified by its "direct hyperscaler partnerships" and its role as a "critical component supplier" to network equipment manufacturers. This dual approach ensures broad market reach and deep integration into the supply chains of major cloud and AI network operators. The company's focus on energy-efficient, higher-performance photonic solutions aligns perfectly with hyperscalers' sustainability and scalability imperatives, potentially enabling margin upside through premium pricing and product differentiation as new platforms scale.

The company is not just selling components; it's enabling new paradigms in optical networking. CEO Michael Hurlston highlighted the "massive potential of OCS and CPO" and teased a "fourth growth driver... poised to be a generational game-changer for the industry: optical scale-up." This forward-looking strategy, combined with a strong balance sheet featuring $1.16 billion in cash and short-term investments, provides Lumentum with significant liquidity to fund ongoing capacity expansion and R&D, ensuring it maintains its technological edge in a rapidly evolving market.

What Does the Analyst Community Say About Lumentum's Valuation and Future?

The analyst community holds a largely bullish view on Lumentum, with a consensus "Buy" rating from 24 analysts (1 Strong Buy, 16 Buy, 7 Hold). However, there's a notable divergence in price targets, reflecting the complexities of valuing a company at the epicenter of such a transformative technological shift. The consensus price target for LITE stands at $442.27, with a median of $475.00. The high target reaches $645.00, while the low is $220.00. It's crucial to note that LITE's current price of $670.50 already exceeds the high analyst target, suggesting that the market's enthusiasm for Lumentum's AI prospects has outpaced traditional analyst models.

This discrepancy often arises when a company experiences rapid, structural growth that fundamentally alters its business model, making historical valuation metrics less relevant. For instance, Lumentum's trailing twelve-month (TTM) P/E ratio is a lofty 189.40, and its P/S ratio is 22.73. While these figures appear stretched compared to traditional tech companies, they reflect investor optimism for Lumentum's pivotal, high-growth role in AI and cloud optical infrastructure. Revenue growth of 21.0% and net income growth of 104.7% year-over-year for FY2025 (TTM) provide some justification for these multiples, but the market is clearly pricing in significant future expansion.

Some valuation models, like a Discounted Cash Flow (DCF) analysis from Simply Wall St, suggest Lumentum could be undervalued by 33.4%, arriving at an intrinsic value of $845.48 per share. This model heavily relies on projected improvements in free cash flow, which analysts forecast to reach $1.52 billion by 2028. Conversely, other narratives suggest the stock is overvalued, with fair value estimates closer to $348.38 to $571.45, implying that the current price already reflects aggressive AI optics assumptions and leaves less room for error.

Despite these valuation debates, the underlying sentiment remains positive. Firms like Mizuho maintain an "Outperform" rating, recognizing Lumentum's role in AI data center advancements. The company's robust Q3 FY26 guidance, with an expected revenue midpoint of $805 million (an 85%+ YoY increase) and EPS of $2.15-$2.35, continues to fuel this optimism. The market is clearly betting on Lumentum's ability to execute on its substantial backlog and new contracts, which are expected to drive sustained growth into 2027 and beyond.

What Are the Risks and Opportunities for Lumentum Investors?

For investors considering Lumentum, the current landscape presents both significant opportunities and inherent risks. The primary opportunity lies in the relentless expansion of AI infrastructure. With hyperscalers pouring hundreds of billions into data centers, Lumentum's core products—Optical Circuit Switches (OCS), Co-Packaged Optics (CPO), and high-speed EMLs—are in structural demand. The company's deep integration with NVIDIA and its "multi-hundred-million-dollar" CPO contract underscore its essential role in this buildout, providing strong revenue visibility and growth catalysts.

Lumentum's ability to expand its gross margin to 33.4% (TTM) and its non-GAAP gross margin to 42.5% in Q2 FY26, up from 32.3% a year prior, highlights improving profitability as AI-driven demand scales. The company's strong cash position of $1.16 billion provides flexibility for strategic investments and capacity expansion, crucial for meeting surging demand. Furthermore, the potential for "optical scale-up" as a "generational game-changer" suggests new avenues for growth beyond current product lines, promising long-term innovation.

However, risks are equally pronounced. Lumentum's valuation, with a TTM P/E of 189.40 and P/S of 22.73, is undeniably rich, implying that a substantial amount of future growth is already priced into the stock. Any slowdown in hyperscaler spending, increased competition, or execution missteps in ramping complex new technologies like OCS and CPO could lead to significant downside. Customer concentration, with heavy reliance on a few hyperscale cloud customers, also poses a risk, making the company vulnerable to shifts in their procurement strategies or internal development efforts.

Operational challenges, such as manufacturing complexity from simultaneously ramping multiple advanced products, and broader macroeconomic or geopolitical factors (e.g., trade restrictions, supply chain issues) could impact costs and component availability. While Lumentum has demonstrated exceptional execution, maintaining this pace in a dynamic environment will be critical. Investors must weigh the immense growth potential driven by AI against the demanding valuation and execution risks inherent in a rapidly evolving technology sector.

Lumentum Holdings stands at a pivotal juncture, uniquely positioned to ride the multi-year wave of AI infrastructure investment. While its stock has seen a meteoric rise, the company's technological leadership and robust financial performance suggest its growth story is far from over. Investors should closely monitor its ability to execute on its substantial backlog and expand its margin profile, as these will be key determinants of its continued success in the AI era.

Want deeper research on any stock? Try Kavout Pro for AI-powered analysis, smart signals, and more. Already a member? Add credits to run more research.