Stock News•3 weeks ago

The Smartest Retirement Strategy You May Not Have Considered

A gradual retirement transition could reduce financial and emotional shock for some workers, though no specific data or magnitude is provided.

Key Takeaways

The traditional "cliff" retirement, where workers abruptly transition from full-time employment to complete leisure, is rapidly becoming a relic of the past. A new paradigm, known as phased retirement, is gaining significant traction, allowing employees to gradually scale back their work hours and responsibilities while still drawing partial benefits and maintaining a connection to the workforce. This shift isn't just a minor adjustment; it represents a fundamental redefinition of what retirement means for millions of Americans and how companies manage their most experienced talent.

This evolving approach offers a compelling middle ground, balancing the desire for continued purpose and financial stability with the need for greater flexibility in later career stages. Workers are increasingly seeking options that allow them to ease into retirement on their own terms, rather than facing an all-or-nothing decision. The data underscores this trend: more than 4 in 10 workers express a desire for wellness programs that include gradual transition opportunities and part-time scheduling.

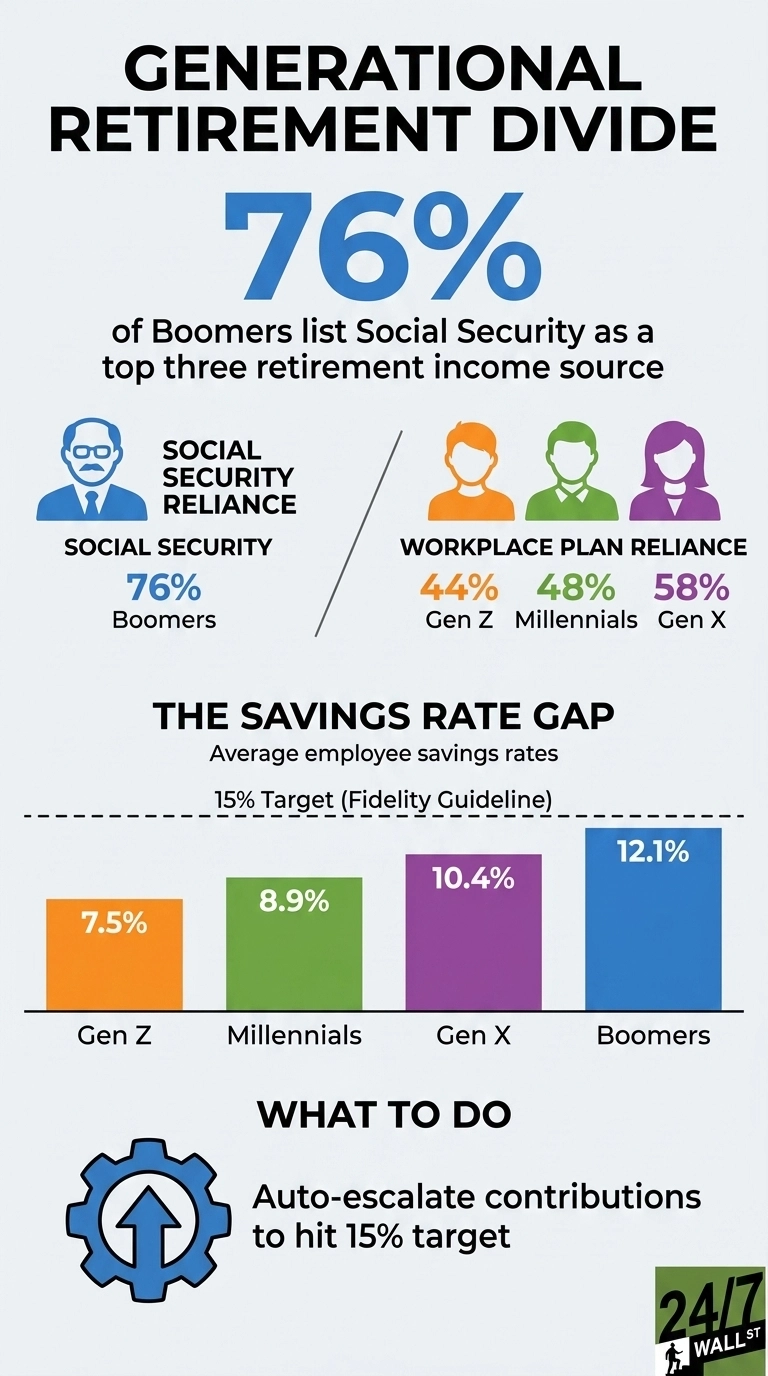

For many, phased retirement isn't merely a preference; it's a financial necessity. Longer life expectancies mean retirement savings must stretch further, often for 20 or 30 years, creating a significant financial gap. Continuing to work, even part-time, helps bridge this gap, allowing individuals to maintain income, delay drawing down savings, and potentially increase Social Security benefits by waiting to claim them. This strategic delay can significantly enhance long-term financial security, making phased retirement a powerful tool in a comprehensive financial plan.

Beyond the financial calculus, there's a profound human element at play. Many older adults find immense value in maintaining a sense of purpose, social engagement, and intellectual stimulation that work provides. Studies even suggest that staying engaged in meaningful work can have positive effects on mental and physical health, offering a smoother emotional and psychological transition compared to an abrupt departure from a lifelong career.

The shift towards phased retirement isn't solely driven by employee demand; it's a strategic imperative for businesses grappling with an aging workforce and a looming talent deficit. As millions of Baby Boomers and older Gen Xers approach traditional retirement age, companies face the daunting prospect of losing invaluable institutional knowledge and expertise. This "brain drain" can severely impact productivity, innovation, and client relationships, making talent retention a top priority.

Phased retirement offers a powerful solution to this challenge. By allowing seasoned employees to reduce their workload while remaining engaged, companies can retain their most experienced workers for longer, leveraging their skills and wisdom to mentor younger generations. This knowledge transfer is critical, especially in highly technical or specialized fields where expertise is built over "years and years" of industry experience. It ensures continuity of operations and helps smooth succession planning, preventing abrupt leadership gaps.

Consider the current labor market dynamics: more than 7 in 10 U.S. employers report struggling to find the skilled workers they need. Simultaneously, birth rates have declined for nearly two decades, meaning fewer young adults are entering the workforce. This demographic reality creates a perfect storm, with the U.S. projected to face its largest labor shortage in history by 2032. Phased retirement directly addresses this by keeping experienced talent in the pipeline, mitigating the impact of a shrinking labor pool.

Furthermore, offering flexible retirement options can significantly boost employee satisfaction and loyalty across all age groups. When younger employees see that their company supports a flexible, humane transition into retirement, it fosters a sense of trust and commitment, making them more likely to stick around for the long haul. This creates a win-win scenario, where employers benefit from retained expertise and a more engaged workforce, while employees gain the flexibility and financial stability they desire.

For individuals contemplating phased retirement, the financial planning implications are multifaceted and require careful consideration. The primary benefit is the ability to prolong income and maintain access to crucial employer-sponsored benefits. Continuing to earn, even at a reduced capacity, can significantly delay the need to tap into retirement savings, allowing those investments more time to grow through compounding. This is particularly vital for Gen Xers, who are the first generation to rely primarily on 401(k)s and personal savings, rather than traditional pensions.

Access to employer-provided health insurance is another critical factor. Many older workers choose to remain employed, even part-time, to maintain health coverage until they become eligible for Medicare at age 65. This can save individuals thousands of dollars annually in premiums and out-of-pocket expenses, providing a crucial financial buffer during a transitional period. Beyond health insurance, benefits like Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs) and employer-sponsored 401(k) matches can continue to provide significant value.

Strategically delaying Social Security claims is another powerful advantage. For every year an individual delays claiming benefits past their full retirement age, up to age 70, their monthly payout increases. Working part-time during a phased retirement allows individuals to bridge the income gap, pushing back their Social Security start date and securing a larger lifetime income stream. This can translate into hundreds, or even thousands, of additional dollars per month in retirement.

Finally, phased retirement provides a valuable opportunity to make final adjustments to one's financial plan. It allows for a "test run" of a reduced income lifestyle, helping individuals fine-tune their budgets and spending habits before fully exiting the workforce. This period can also be used to pay down any remaining debt, ensuring a debt-free transition into full retirement and enhancing overall financial independence.

The retirement landscape is undergoing a significant technological transformation, with AI and predictive planning tools revolutionizing how individuals plan for their golden years and how employers support them. By 2026, AI is expected to become a key driver of personalization, allowing plan participants to simulate various income and longevity scenarios with unprecedented accuracy. These advanced tools move beyond generic advice, offering tailored insights that reflect an individual's unique financial situation, risk tolerance, and lifestyle aspirations.

Employers are increasingly integrating these AI-driven solutions into comprehensive pre-retirement programs. These programs, often delivered through digital and virtual coaching platforms, provide personalized retirement income projections, spending estimates, and education on complex topics like Social Security and Medicare elections. This level of personalized guidance helps make the transition to retirement more predictable, confident, and financially secure for employees, reducing anxiety and improving overall readiness.

Beyond individual planning, technology is expanding access to workplace retirement savings, particularly for small businesses. Fintech-powered recordkeeping platforms are bringing low-cost scalability to smaller employers, making it easier and more affordable to offer robust retirement plans. This, combined with legislative incentives from the SECURE Acts, is driving the growth of multiple-employer plans (MEPs) and pooled-employer plans (PEPs), which streamline administration and fiduciary oversight, further democratizing access to retirement savings.

The digital evolution also extends to financial wellness benefits, which are becoming a standard offering. Companies are expanding beyond traditional retirement plans to promote holistic financial health, integrating everything from debt counseling to personalized savings dashboards. This trend recognizes that financial stress impacts job performance and that younger workers, in particular, expect financial education and support from their employers. By 2026, 3 out of 4 employers plan to add wellness programs, signaling a major mindset shift where retirement planning is seen as a key component of overall employee well-being.

Policy changes, particularly the ongoing implementation of the SECURE Act 2.0, are fundamentally reshaping retirement contributions and plan design. With full enforcement expected by mid-2026, these updates are driving significant improvements in employee participation and the creation of new retirement plans. Key changes include bigger catch-up limits indexed to inflation, mandatory Roth catch-ups for higher earners, and automatic enrollment for new 401(k) and 403(b) plans. Furthermore, startup credits covering up to 100% of setup costs are encouraging more small businesses to offer retirement benefits, expanding coverage for millions of Americans.

Investment trends are also evolving, with Environmental, Social, and Governance (ESG) investing playing an increasingly prominent role, especially among younger generations. By 2026, over 40% of new plan participants are expected to prefer ESG or sustainable investment funds. Employers offering ESG options are seeing higher engagement, highlighting how values now drive financial decisions and influencing modern pension plan design. This shift reflects a broader societal demand for investments that align with personal ethics, pushing asset managers and plan sponsors to adapt their offerings.

The demand for guaranteed income options is another significant trend. Retirees are increasingly seeking income stability over market-dependent returns, leading more 401(k)s and pension plans to add in-plan annuities and lifetime income products. Since 2023, there has been a 45% growth in plans offering annuity features, with lifetime income illustrations now standard on plan statements. This widespread adoption is supported by new legislation, making these income strategies among the most practical for converting savings into lifelong security.

Finally, the growth of state-run retirement programs is expanding access nationwide. By 2026, over 20 U.S. states are likely to mandate employer access to retirement savings plans, often through auto-IRA programs for uncovered workers. This initiative not only expands coverage for small business employees but also encourages employers to adopt private 401(k)s or pensions, significantly boosting overall national retirement participation and closing the coverage gap for millions of Americans.

The convergence of these trends—phased retirement, technological innovation, and policy shifts—presents a dynamic landscape for investors and the broader economy. For companies, the ability to effectively implement phased retirement programs and leverage experienced workers will be a key competitive advantage, impacting talent retention, productivity, and ultimately, shareholder value. Investors should scrutinize how companies are adapting their human capital strategies to navigate the aging workforce and talent shortages.

The expansion of retirement plan access and the growing preference for ESG investments also signal significant opportunities for financial service providers and asset managers. Firms that can offer personalized, AI-driven planning tools, robust ESG options, and integrated guaranteed income solutions are well-positioned for growth. The increasing complexity of retirement planning, coupled with greater individual responsibility, will drive demand for sophisticated advisory services and innovative product offerings.

Economically, a workforce that phases into retirement rather than abruptly exits can mitigate the impact of labor shortages and maintain higher levels of consumer spending. Older workers who remain engaged contribute to the tax base, delay drawing full Social Security benefits, and often continue to save, providing a stabilizing force. This gradual transition supports economic continuity and reduces the strain on social safety nets, fostering a more resilient financial ecosystem.

Ultimately, the future of retirement is one of flexibility, personalization, and sustained engagement. Investors should recognize that these shifts are not merely demographic curiosities but fundamental structural changes that will influence corporate performance, market trends, and the financial well-being of a generation. Understanding these dynamics is essential for making informed investment decisions and preparing for the evolving economic landscape.

The retirement landscape is undergoing a profound transformation, moving from a rigid cliff to a flexible slope. For both individuals and employers, embracing phased retirement and leveraging technological advancements will be crucial for navigating this new era of financial security and workforce stability. Proactive planning and adaptability are no longer optional, but essential for thriving in the evolving world of work and retirement.

Want deeper research on any stock? Try Kavout Pro for AI-powered analysis, smart signals, and more. Already a member? Add credits to run more research.