Stock News•3 weeks ago

I'm No Longer Focused on Funding My 401(k). Here's Why.

A saver shifts strategy away from 401(k) funding, citing personal reasons for the change.

Key Takeaways

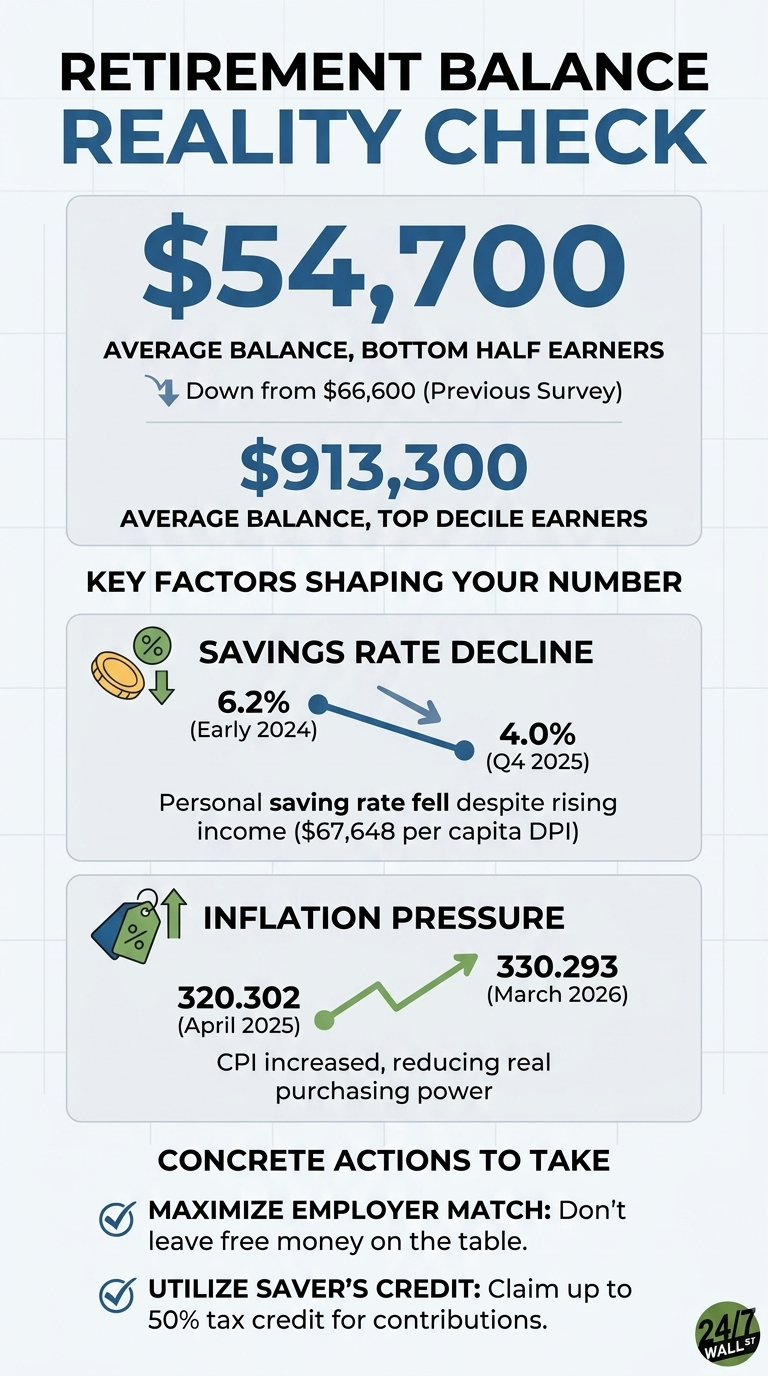

Americans are increasingly turning to their retirement savings as an emergency fund, with a record number of individuals making hardship withdrawals from their 401(k) accounts. Data from Vanguard Group reveals that 6% of participants in plans it administers took hardship withdrawals in 2025, a sharp increase from 4.8% in 2024 and more than triple the pre-pandemic average of roughly 2%. This trend isn't just a blip; it marks the sixth consecutive year of rising hardship withdrawals, painting a clear picture of escalating financial strain across the country.

The reasons behind this surge are stark and reflect fundamental challenges in household finances. The primary drivers for these withdrawals are often critical, life-altering events. Avoiding foreclosure or eviction accounts for a substantial 36% of withdrawals, while medical expenses represent another 31%. Other significant factors include tuition costs at 13%, primary residence repairs at 11%, and even primary residence purchases at 5%. The median withdrawal amount, according to Vanguard, was a modest $1,900, indicating these aren't large-scale raids but rather desperate measures to cover immediate, unavoidable costs.

This phenomenon highlights a troubling paradox: while average 401(k) account balances rose by 13% in 2025 due to positive market performance, a significant portion of the workforce is simultaneously struggling to meet basic financial obligations. The retirement savings system, designed for long-term wealth accumulation, is increasingly being pressed into service as a short-term safety net. This dual reality underscores a widening gap in financial stability, where market gains benefit some, but a growing segment of the population faces acute, immediate financial pressures.

The ease of accessing these funds has also played a role. Congress reformed the process for 401(k) hardship withdrawals in 2018, making it simpler by removing the requirement that participants first take a loan before being allowed a withdrawal. This legislative change, coupled with automatic enrollment helping more workers, especially lower-income individuals, save for retirement, means that more people now have a 401(k) to tap into when emergencies strike. While intended to provide a safety valve, it also creates a path of least resistance for those facing dire circumstances.

The rising tide of 401(k) hardship withdrawals isn't happening in a vacuum; it's a direct symptom of broader economic pressures squeezing American households. Persistent inflation, which has eroded purchasing power over the past few years, means that everyday expenses like groceries, utilities, and housing consume a larger portion of household budgets. When unexpected costs arise, many families find their cash reserves quickly depleted, leaving them with few options beyond their retirement accounts. This is particularly true for lower-income and hourly workers, who are disproportionately represented among those taking early withdrawals.

High interest rates have compounded the problem, making traditional borrowing alternatives like personal loans or credit card advances significantly more expensive. National credit card balances have already surpassed $1 trillion, with delinquency rates on the rise, especially among vulnerable households. For individuals already struggling with debt, taking on more high-interest credit is often not a viable solution, pushing them towards their 401(k) as the only accessible pool of funds. The flat usage of 401(k) loans, which remain below pre-pandemic levels, suggests that even this more favorable borrowing option isn't always sufficient or preferred over an outright withdrawal when facing severe hardship.

A critical underlying issue is the widespread lack of adequate emergency savings. Many Americans simply don't have enough liquid assets to cover three to six months of living expenses, let alone a sudden medical bill or home repair. When an emergency strikes, the 401(k), despite its long-term purpose, becomes the de facto emergency fund. This reliance on retirement savings for immediate needs highlights a systemic vulnerability in personal finance, where the line between long-term investment and short-term survival has blurred.

Michael Eisenga, CEO of First American Properties, aptly described this trend as "a flashing red light for the American economy." He noted that when nearly 5% of participants are tapping retirement accounts in a single year, it's not about discretionary spending but rather a clear indicator of financial distress. This sentiment is echoed by experts who point to the "leakage" from 401(k) plans – the erosion of retirement assets due to early distributions – as a significant threat to long-term wealth accumulation and a driver of wealth inequality.

Tapping into a 401(k) early, even for legitimate hardships, carries significant long-term consequences that can severely jeopardize an individual's retirement security. The most immediate impact is the permanent reduction of the account balance. Every dollar withdrawn is a dollar that will not benefit from the power of compound interest over decades. For instance, a $1,900 withdrawal today could easily represent tens of thousands of dollars in lost growth by retirement age, especially for younger workers. The IRS itself warns that "the amount of the hardship distribution will permanently reduce the amount you’ll have in the plan at retirement."

Beyond the lost compounding, early withdrawals often trigger penalties and taxes. For those under 59½, a 10% early withdrawal penalty typically applies, on top of the amount being taxed as ordinary income. This means a $1,900 withdrawal could see hundreds of dollars immediately vanish to penalties and taxes, further reducing the net amount received and exacerbating the financial hole. While some recent legislation, like SECURE 2.0, has introduced limited penalty-free withdrawals for specific emergencies, these are generally capped at small amounts like $1,000 and don't negate the tax implications or the fundamental loss of future growth.

This "leakage" from 401(k) plans is a growing concern for plan sponsors and financial experts alike. It's not just about hardship withdrawals; roughly one-third to more than 40% of workers changing jobs choose to liquidate their 401(k) balances rather than roll them over, compounding long-term losses. This consistent erosion of retirement assets undermines the very purpose of the defined contribution system, which was designed to fund retirement, not to manage short-term financial shocks.

The cumulative effect of these withdrawals contributes to a broader crisis in retirement readiness. A recent AARP survey found that more than 20% of adults aged 50 and older have no retirement savings at all. When even those who do save are forced to deplete their accounts early, it creates a demographic cohort increasingly reliant on social safety nets in their later years. This trend exacerbates long-term wealth inequality, particularly impacting lower-income households who are more likely to face the financial emergencies that necessitate these difficult choices.

The increasing ease of accessing 401(k) funds, driven by legislative changes and evolving plan designs, has undeniably contributed to the uptick in hardship withdrawals. Prior to 2018, plan participants were often required to exhaust all available 401(k) loan options before being permitted to take a hardship withdrawal. The Bipartisan Budget Act of 2018 eliminated this mandatory requirement, making it optional for employer plans. This change effectively removed a significant hurdle, making hardship withdrawals a more immediate and less complicated option for those in distress.

Further legislative shifts under the SECURE 2.0 Act of 2022 have continued this trend, albeit with some guardrails. This law allows employees to self-certify that they have experienced a "safe harbor event" qualifying for a hardship withdrawal, reducing the administrative burden on plan administrators. SECURE 2.0 also introduced provisions for penalty-free withdrawals of up to $1,000 once every three years for specific emergency needs, with the option to repay it within three years to avoid a tax bill. While these measures aim to provide flexibility, they also normalize the idea of tapping into retirement funds for non-retirement purposes.

The paradox of automatic enrollment also plays a role. While automatic contributions have significantly boosted savings and investment outcomes, especially for lower-income workers, they have also brought more individuals into the 401(k) system who might not have robust emergency savings outside of it. As Vanguard noted, "Given that it's now easier to request a hardship withdrawal and that automatic enrollment is helping more workers save for retirement, especially lower-income workers, a modest increase isn't surprising." For a subset of these workers, the 401(k) becomes the only available safety net.

However, the distinction between 401(k) loans and hardship withdrawals remains critical. Loans, while still drawing from retirement funds, allow participants to repay the money, often with interest that goes back into their own account, thus mitigating the long-term impact. Hardship withdrawals, by contrast, are permanent. The fact that 401(k) loan usage has remained flat and below pre-pandemic levels, even as hardship withdrawals soar, suggests that for many, the need is so urgent that they bypass the loan option entirely, opting for the immediate, albeit more damaging, withdrawal.

Given the alarming trend of 401(k) hardship withdrawals, individuals must proactively implement strategies to safeguard their retirement savings and build financial resilience. The most crucial step is establishing a dedicated emergency savings fund outside of retirement accounts. Financial experts typically recommend saving at least three to six months' worth of essential living expenses in an easily accessible, liquid account, such as a high-yield savings account. This buffer can absorb unexpected costs like medical bills or job loss, preventing the need to raid long-term investments.

For those whose employers offer it, utilizing emergency savings accounts linked to retirement plans, as introduced by SECURE 2.0, can be a game-changer. These accounts allow employees to contribute up to $2,500 to an emergency fund that is paired with their retirement plan, providing access to short-term savings without touching the 401(k). While these features have been slow to gain traction, they represent a valuable tool for building a financial cushion and preventing "leakage" from retirement funds.

Beyond emergency savings, a holistic approach to financial wellness is essential. This includes creating and sticking to a budget to manage daily expenditures, actively working to reduce high-interest debt like credit card balances, and exploring alternatives to 401(k) withdrawals when facing hardship. For instance, if facing mortgage difficulties, refinancing or negotiating payment delays with lenders should be explored before tapping retirement funds. Similarly, for medical expenses, payment plans or assistance programs might be available.

Finally, individuals should regularly review their 401(k) contribution rates. While financial stress is real, many participants are still increasing their deferral rates, either on their own or through automatic annual increases. This commitment to consistent saving, even small increments, can significantly impact long-term growth. Advisors are in a unique position to counsel participants, emphasizing that unless in dire circumstances, taking a withdrawal after market drops locks in losses and sacrifices future gains. The goal is to keep retirement money invested for its intended purpose.

The record surge in 401(k) hardship withdrawals is a stark reminder of the financial fragility many Americans face, despite overall market gains. It underscores the urgent need for individuals to prioritize building robust emergency savings and for employers to support comprehensive financial wellness programs. While legislative changes have made accessing funds easier, the long-term cost to retirement security is substantial.

Ultimately, the goal is to ensure that 401(k)s can fulfill their primary mission: providing a secure retirement. This requires a concerted effort from individuals, employers, and policymakers to strengthen financial foundations and prevent retirement accounts from becoming the default emergency fund.

Want deeper research on any stock? Try Kavout Pro for AI-powered analysis, smart signals, and more. Already a member? Add credits to run more research.