Key Takeaways

- Rivian Automotive (RIVN) demonstrated significant progress in 2025, achieving positive consolidated gross profit for the first time, driven by strong software and services growth and cost reductions.

- The upcoming R2 platform, priced at around $45,000, is a crucial catalyst for expanding Rivian's market reach and is expected to drive substantial delivery growth in 2026 and beyond.

- Despite narrowing losses and improving operational efficiency, Rivian continues to burn significant cash, necessitating careful management of its $6.08 billion liquidity to fund ambitious growth plans and navigate a competitive EV landscape.

Is Rivian Automotive (RIVN) Finally Turning the Corner on Profitability?

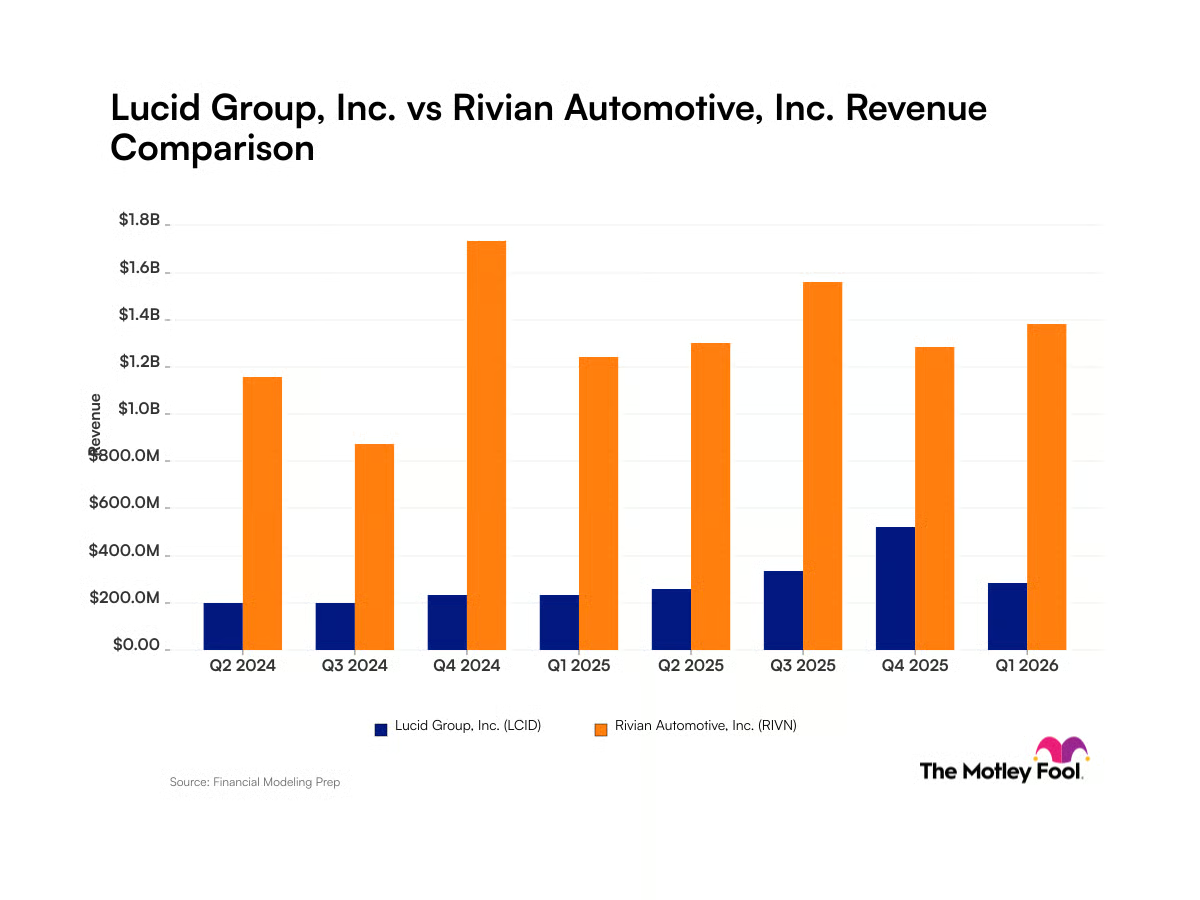

Rivian Automotive has shown tangible signs of progress, with its 2025 financial results marking a pivotal shift towards operational efficiency and a clearer path to profitability. The company reported full-year 2025 revenue of $5.387 billion, an 8% increase over 2024, and, more importantly, swung to a consolidated gross profit of $144 million from a substantial (1.2)billion∗∗lossintheprioryear.This∗∗1.3 billion year-over-year improvement is a testament to management's focus on pricing strategies, cost reductions, and the burgeoning software and services segment.

While the overall net loss for 2025 still stood at (3.626)billion∗∗,anotableimprovementfrom∗∗(4.746) billion in 2024, the positive gross profit signals a fundamental strengthening of the business model. The fourth quarter of 2025 further underscored this trend, with revenue reaching $1.286 billion and a consolidated gross profit of $120 million. This performance beat analyst expectations for loss per share, coming in at (0.66)∗∗againstananticipated∗∗(0.68), providing a much-needed boost to investor confidence.

The underlying story here is a strategic pivot. Rivian's automotive segment, while improving, still posted a negative gross profit of (432)million∗∗in2025.However,thesoftwareandservicesdivisionhasemergedasahigh−marginpowerhouse,generating∗∗1.557 billion in revenue and a remarkable $576 million in gross profit for 2025, a significant leap from $7 million in 2024. This growth, partly fueled by the Volkswagen Group joint venture, highlights a diversified revenue stream that could de-risk the company's reliance solely on vehicle sales and accelerate its journey to sustainable profitability.

The company's guidance for 2026 anticipates continued heavy investment, with adjusted EBITDA projected between (2.10)billion∗∗and∗∗(1.80) billion, and capital expenditures between $1.95 billion and $2.05 billion. This indicates that while gross margins are improving, Rivian is still in a significant growth phase, pouring resources into scaling production and developing future vehicle programs like the R2. The challenge remains balancing aggressive expansion with the imperative to stem cash burn and achieve overall net profitability.

What Does the R2 Launch Mean for Rivian's Future?

The upcoming launch of the R2 platform is arguably the most critical catalyst for Rivian's long-term success, representing a strategic pivot to a broader, more accessible market segment. Positioned with a starting price of around $45,000, the R2 is designed to appeal to a significantly wider audience than the premium R1 series, which starts at approximately $77,000. This move is a direct response to the market's hunger for a mid-sized SUV that combines robust technology, autonomous capabilities, and a reasonable price point, a segment currently underserved by competitors.

Rivian's management has explicitly stated that 2026 will be an "inflection point" for the business, with the R2 expected to become the "majority of the volume" by the end of 2027 as production ramps up. The company has guided for 62,000–67,000 vehicle deliveries in 2026, representing a substantial 47% to 59% increase from the 42,247 units delivered in 2025. This ambitious forecast hinges heavily on the successful introduction and scaling of the R2, with initial production starting with a single shift and plans to add a second shift by year-end and a third in 2027.

The R2's success is not just about unit volume; it's about improving the automotive segment's gross margins. While the R1 was a premium offering, the R2's design and manufacturing efficiencies are expected to lower the bill of materials, supporting a path toward stronger margins over time. Rivian has set an ambitious goal of achieving a 20% automotive gross margin in 2027 and an overall company gross margin above 25%, targets that are largely dependent on the R2's cost structure and production scale.

However, the transition won't be without its challenges. Management anticipates that the R2 launch will negatively impact gross margins in the second and third quarters of 2026 before improving in the final quarter as production scales. This temporary dip underscores the inherent risks in new model introductions, including potential production setbacks, supply chain disruptions, and the need for significant capital expenditure. Despite these hurdles, the R2 represents Rivian's most promising avenue for achieving sustained growth and profitability in a competitive EV market.

How Strong is Rivian's Balance Sheet Amidst Persistent Cash Burn?

Rivian's balance sheet presents a mixed picture: a robust cash position provides a lifeline for its ambitious growth, yet the persistent cash burn remains a significant concern for investors. The company ended 2025 with $6.08 billion in cash, cash equivalents, and short-term investments, with total liquidity, including its asset-based revolving credit facility, standing at $6.588 billion. This substantial war chest is critical, as Rivian continues to operate at a significant loss and requires heavy investment to scale production and develop new models.

Despite the positive consolidated gross profit in 2025, Rivian's adjusted EBITDA was a negative (2.063)billion∗∗,andfreecashflowremaineddeeplyintheredat∗∗(2.489) billion. The guidance for 2026 projects adjusted EBITDA losses between (1.80)billion∗∗and∗∗(2.10) billion, alongside capital expenditures of $1.95 billion to $2.05 billion. These figures clearly indicate that the company will continue to consume a substantial amount of cash in the near term, highlighting the importance of its current liquidity to bridge the gap to profitability.

The cash burn rate, while still high, has shown some improvement. Net cash used in operating activities decreased from (1.716)billion∗∗in2024to∗∗(779) million in 2025, and free cash flow improved from (2.857)billion∗∗to∗∗(2.489) billion. This indicates that operational efficiencies and gross margin improvements are starting to translate into a slower rate of cash depletion. However, the Q4 2025 free cash outflow of $(1.14) billion was a stark reminder of the capital-intensive nature of the automotive business, especially during new product ramps.

Shareholder dilution is another factor to consider. The weighted-average common shares outstanding increased from 1.058 billion in Q4 2024 to 1.233 billion in Q4 2025, reflecting the company's reliance on equity financing to fund its operations. While a strong cash position offers a buffer against immediate liquidity crises, sustained cash burn without a clear path to self-sufficiency will inevitably lead to further dilution or increased debt, both of which can pressure shareholder value. Investors must weigh the company's impressive liquidity against its ongoing need for capital and the potential for future financing activities.

Is RIVN Stock "Outrageously Cheap" or Still Overvalued?

The valuation of Rivian stock presents a fascinating dichotomy, with some analysts labeling it "outrageously cheap" while others point to traditional metrics suggesting overvaluation. This divergence stems from the company's unique position as a high-growth EV startup still in its heavy investment phase, making conventional valuation methods challenging. The stock has experienced significant volatility, with a 22.9% decline over 30 days and a 24.0% decline year-to-date as of February 2026, yet it still returned 18.3% over the last year.

One perspective, often supported by Discounted Cash Flow (DCF) analysis, suggests Rivian is significantly undervalued. A DCF model, which projects future cash flows and discounts them back to today, estimated an intrinsic value of $41.18 per share, implying the stock is 64.2% undervalued relative to its current price. This model typically assumes free cash flow will turn positive over time, reaching $1.97 billion by 2030, after several years of negative cash flow. This bullish view often emphasizes the long-term potential of the R2 platform, manufacturing efficiencies, and high-margin software revenues.

Conversely, Price-to-Sales (P/S) ratios paint a different picture. Rivian currently trades at a P/S of 3.48x, which is considerably higher than the auto industry average of 0.58x and its peer group average of 1.75x. Simply Wall St's proprietary "Fair Ratio" for Rivian, which accounts for growth profile, profit margins, industry, market cap, and risks, stands at 1.24x. Comparing the current 3.48x P/S to this 1.24x Fair Ratio suggests the shares are pricing in more optimistic assumptions than the model implies, leading to an "OVERVALUED" conclusion on this metric.

Analyst ratings are also split, reflecting the complexity. While some firms like Stifel and Needham & Company raised their price targets to $20 and $23 respectively, giving "Buy" ratings, others like D.A. Davidson downgraded the stock to "Underperform" with a $14 target. The consensus rating from 20 analysts is a "Buy," with a mean target price of $18.10, indicating a potential upside of over 17% from current levels. This mixed sentiment underscores that Rivian remains a speculative investment, with its valuation heavily dependent on future execution and the successful transition to profitability.

What Are the Key Risks and Opportunities for RIVN Investors?

Investing in Rivian at this juncture involves navigating a landscape rich with both transformative opportunities and significant, inherent risks. On the opportunity side, the launch of the R2 platform is a game-changer. Its $45,000 price point and mid-sized SUV form factor tap into a massive, underserved market, potentially driving exponential delivery growth and market share expansion. The Volkswagen Group joint venture further validates Rivian's technology and provides a high-margin revenue stream from software and services, diversifying its business model beyond just vehicle sales.

Furthermore, Rivian's commitment to technology leadership, including advancements in autonomy and battery systems, positions it well for long-term competitive advantage. The company's improving operational efficiency, evidenced by the positive consolidated gross profit in 2025 and shrinking automotive gross losses, suggests a management team capable of executing on cost reductions and scaling production. If Rivian can achieve its ambitious 20% automotive gross margin and 25%+ overall gross margin targets by 2027, the current valuation could indeed appear "cheap" in retrospect.

However, the risks are equally substantial. The most pressing concern remains the continued heavy cash burn. Despite narrowing losses, Rivian is still projected to burn billions in adjusted EBITDA and capital expenditures in 2026. This necessitates careful management of its $6.08 billion cash reserves and raises the specter of future capital raises, which could lead to further shareholder dilution. The EV market is also intensely competitive, with established players like Tesla and traditional automakers aggressively expanding their electric offerings, potentially pressuring Rivian's pricing and market share.

Production setbacks at its Normal, Illinois factory, supply chain disruptions, and macroeconomic headwinds like higher interest rates and reduced policy support for EVs could all derail Rivian's growth plans. The success of the R2 is not guaranteed, and any delays or lukewarm reception could severely impact its financial trajectory. Moreover, regulatory credit sales, which contributed to its gross profit, might face headwinds as legacy automakers become less reliant on purchasing them. Investors must weigh Rivian's innovative potential and strategic execution against these formidable operational and market challenges.

How Should Investors Position Themselves for Rivian's "Inflection Year"?

For investors considering Rivian, 2026 is undeniably a "transition year" and an "inflection point," demanding a nuanced approach. The company's recent financial improvements, particularly the swing to positive consolidated gross profit and the burgeoning software and services segment, offer a compelling long-term narrative. The R2 launch, with its accessible price point and significant market potential, is the primary catalyst to watch, promising substantial delivery growth and a path to improved margins.

However, the journey will remain volatile. Rivian's continued heavy cash burn and projected adjusted EBITDA losses for 2026 mean it is not yet a self-sustaining enterprise. Risk-tolerant investors might consider a small, speculative position, recognizing the significant upside potential if the R2 launch is successful and the company executes on its profitability targets. Conversely, more conservative investors might prefer to remain on the sidelines, awaiting clearer signs of sustained positive free cash flow and a more stable competitive landscape before committing capital.

The stock's current valuation, which appears cheap on a DCF basis but expensive on P/S multiples, reflects this inherent uncertainty. Monitoring R2 production ramp-up, automotive gross margin progression, and the rate of cash burn will be crucial metrics for assessing Rivian's progress throughout 2026. Ultimately, Rivian remains a high-risk, high-reward proposition, where patient investors with a long-term horizon and a strong conviction in the company's vision could be rewarded, but only if management successfully navigates the challenging road ahead.

Want deeper research on any stock? Try Kavout Pro for AI-powered analysis, smart signals, and more. Already a member? Add credits to run more research.