Stock News•1 week ago

Can AST SpaceMobile's Upcoming Satellite Launch Advance Connectivity?

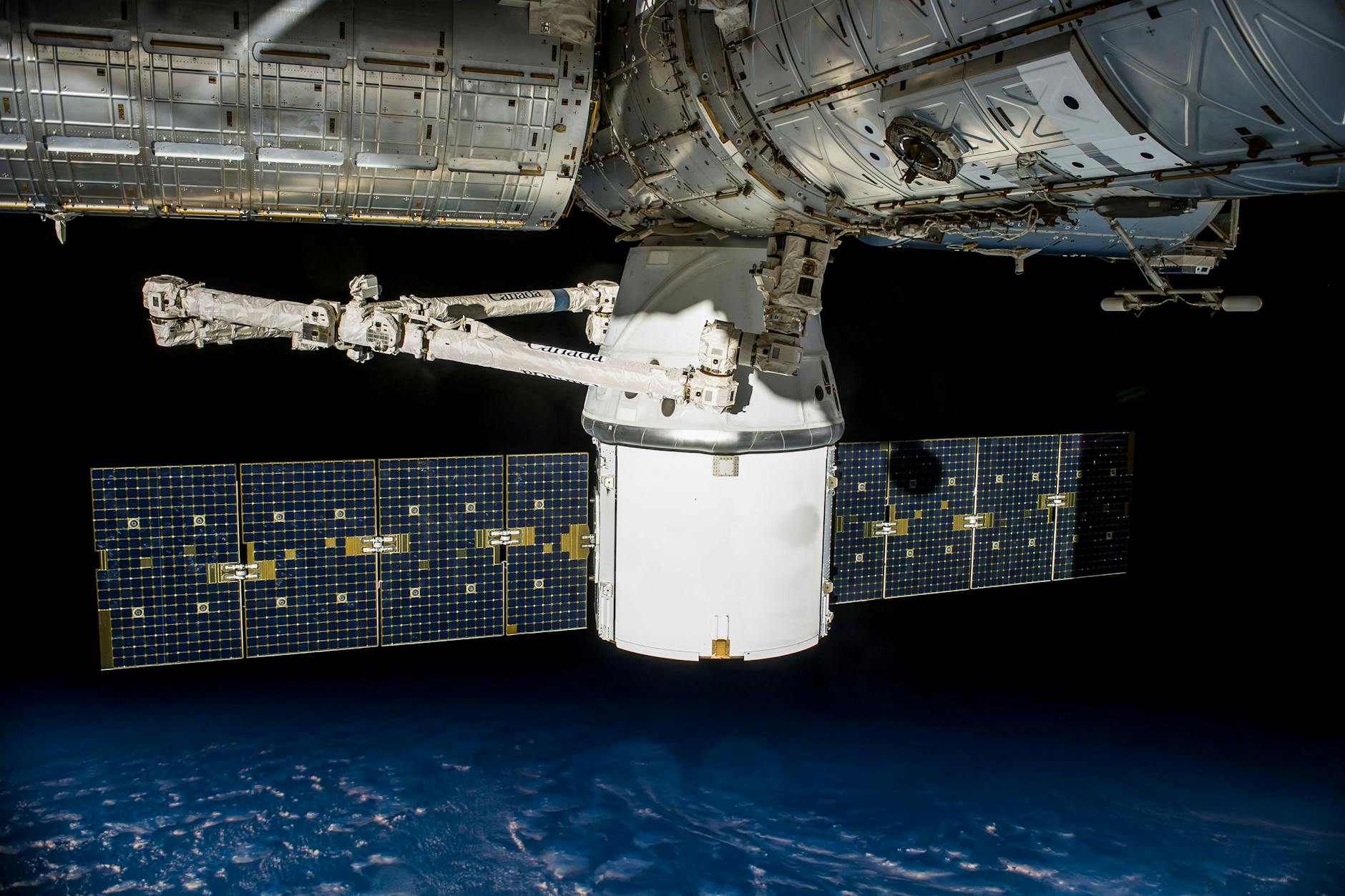

AST SpaceMobile's June 17, 2026 Falcon 9 launch will deploy BlueBird satellites 8–10, scaling its direct-to-smartphone cellular broadband network.

Key Takeaways

Yes, the direct-to-device (D2D) satellite-to-cell race is fundamentally reshaping the telecommunications landscape, moving from theoretical promise to commercial reality in 2026. This shift is driven by a critical need to eliminate coverage gaps, enhance network resilience, and unlock new revenue streams, pushing traditional carriers into strategic alliances with Low Earth Orbit (LEO) satellite providers. The convergence of terrestrial and non-terrestrial networks (NTN) is no longer a distant vision but an active battleground for market share and technological leadership.

Major players like Verizon, Deutsche Telekom, and Orange are at the forefront of this evolution, recognizing that seamless connectivity, regardless of location, is becoming a core differentiator. These partnerships are designed to extend premium cellular services to remote areas, disaster-prone regions, and even maritime or aviation sectors without requiring specialized hardware. This strategic pivot is a direct response to evolving customer expectations and the increasing demand for "always-on" connectivity, even in the most challenging environments.

The stakes are high, with the global satellite internet market projected to reach $22.6 billion by 2030, attracting significant capital and innovation. Companies like AST SpaceMobile and Starlink are deploying vast constellations of LEO satellites, effectively creating "cellular access from space" that integrates directly with existing mobile networks. This technological leap promises to democratize mobile connectivity in underserved areas, but it also introduces complex challenges related to spectrum policy, network integration, and scalability.

Ultimately, the success of this satellite-to-cell paradigm hinges on the ability of these partnerships to deliver reliable, high-capacity services at competitive price points. It's a delicate balance between aggressive deployment schedules, managing substantial capital expenditures, and navigating a rapidly evolving regulatory environment. The coming years will reveal which alliances can effectively bridge the gap between space-based innovation and terrestrial network demands, setting the stage for the next era of global connectivity.

Major carriers are adapting by strategically partnering with satellite providers to extend their network reach and enhance service offerings, rather than attempting to build out their own LEO constellations from scratch. This collaborative approach allows them to leverage existing satellite technology and expertise, rapidly addressing coverage gaps and improving network resilience without the prohibitive costs and time associated with dense terrestrial infrastructure buildouts. Verizon's definitive commercial agreement with AST SpaceMobile is a prime example of this strategy, aiming to deliver space-based cellular coverage in the U.S. starting in 2026.

This partnership enables Verizon subscribers to connect to AST SpaceMobile’s LEO satellites using standard, unmodified phones, extending Verizon’s premium 850 MHz low-band spectrum into remote areas. The deal, which includes a $100 million commitment from Verizon, solidifies a relationship that had previously been under speculation, with some industry watchers wondering if Verizon might instead tap SpaceX for its cellular Starlink service. This move protects Verizon's high-end brand positioning and enterprise accounts by offering a "coverage assurance" layer, putting pressure on rivals to firm up their own non-terrestrial network (NTN) roadmaps.

Similarly, other global telecom giants like Deutsche Telekom and Orange are also engaging in satellite partnerships to expand their mobile network coverage. While specific details on Deutsche Telekom's and Orange's direct-to-cell satellite partnerships were not extensively detailed in the provided context, the broader industry trend indicates a clear move towards such alliances. For instance, T-Mobile has famously partnered with Starlink for its T-Satellite service, which now supports data for apps like WhatsApp and location sharing, in addition to text messaging, across rival carriers.

These strategic alliances are critical for carriers to unlock novel use cases, differentiate their 5G offerings, and future-proof their infrastructure in an increasingly competitive market. The focus is on seamless integration into the mobile core, ensuring policy control, emergency services, and lawful intercept capabilities meet carrier-grade norms. This collaborative model signals a shift from competition to integration, where satellite networks complement existing terrestrial infrastructure rather than making it obsolete, filling gaps and enabling use cases that traditional infrastructure cannot economically address.

For satellite innovators like AST SpaceMobile (ASTSW) and Starlink, the investment implications are substantial, characterized by high growth potential, significant capital demands, and a nuanced risk-reward profile. AST SpaceMobile, trading at $13.50 with a market cap of $1.75 billion, has seen its stock surge on news of definitive commercial agreements, such as the one with Verizon, which investors view as validation of its model and a clearer line of sight to revenue. The company plans to launch 45–60 satellites by 2026 to support commercial broadband connectivity to unmodified smartphones, with over 50 mobile network operators as partners, covering nearly 3 billion subscribers.

However, AST SpaceMobile remains largely pre-revenue, generating modest income primarily through government contracts and early-stage licensing agreements. While Q3 revenue in 2025 reached $14.74 million, a 1,236% gain year-over-year, it still fell short of analyst expectations of $22.04 million. The company's aggressive capital expenditures to build out its global cellular broadband network from space, coupled with a high price-to-sales ratio, raise questions about valuation sustainability and future performance. Investors are closely monitoring satellite deployment, revenue momentum, cost efficiency, and partnership expansion to validate its current valuation.

Starlink, while not publicly traded as a standalone entity (it's part of SpaceX, valued at $400 billion in 2025 with a potential IPO in 2026-2027), demonstrates the immense scale and market dominance achievable in the LEO sector. It generated $11.8 billion in revenue by 2025, boasts over 9 million subscribers, and operates 60% of all active satellites, holding 90% of the satellite internet market. Starlink's direct-to-cell service, rebranded as Starlink Mobile, aims for "broadband connectivity to hundreds of millions of phones globally," with 16 million users currently.

Despite Starlink's impressive growth, both companies face significant challenges. These include regulatory hurdles, spectrum allocation complexities, geopolitical risks, and the operational strain of managing vast, short-lifespan satellite fleets. Starlink's satellites have a lifespan of just five years, necessitating continuous and costly replacements, and network congestion has led to $100 to $250 congestion fees. For investors, these innovators offer high-reward potential but demand careful consideration of execution risks, capital deployment efficiency, and the long-term competitive landscape, especially as Amazon's Project Kuiper and other government-backed constellations intensify the LEO race.

The broader competitive dynamics in the telecom sector are intensifying, marked by a dual focus on expanding ubiquitous connectivity and aggressively managing costs. Traditional carriers like Verizon (VZ, trading at $50.87 with a market cap of $214.55 billion) are under immense pressure to maintain profitability while investing heavily in next-generation networks and services. This environment is forcing a re-evaluation of long-standing expenditures, such as major sports sponsorships, to free up capital for strategic initiatives like satellite partnerships.

Cost pressures are a significant driver behind these strategic shifts. While the provided context mentions Verizon considering divesting its NFL sponsorship to save money, it's a clear indicator of the broader industry trend to optimize spending. Telecom operators are facing eroding customer satisfaction and loyalty, with up to 77% of consumers feeling no loyalty to their provider and annual churn rates around 22%. Despite massive investments in fiber and 5G expansion, customers perceive little meaningful differentiation, making cost-efficiency and unique service offerings paramount.

The rise of LEO satellite providers like Starlink and AST SpaceMobile introduces a new layer of competition, particularly in underserved markets. While these satellite services are often positioned as complementary to terrestrial networks, they also represent a potential threat to traditional revenue streams, especially if they offer more affordable subscription models in developing regions. Amazon's Leo Ultra, for instance, is touting 400 Mbps upload and 1 Gbps download speeds and private access to AWS, with plans for more accessible home and small business offerings.

This competitive landscape is also pushing carriers to diversify beyond basic connectivity, moving towards a "telco to techco" model. This involves exploring emerging opportunities in network APIs, AI, and data services, which, while small in 2026, could become material over time. AI, in particular, is reshaping enterprise network design and operations, enabling automated provisioning and self-healing networks. The challenge for carriers is to balance these innovative, high-capital ventures with the need to maintain solid margins in a mature, low-growth industry primarily driven by basic consumer connectivity.

Apple's role, alongside other device manufacturers, will be pivotal in shaping the future of connectivity, particularly as direct-to-device (D2D) satellite services become mainstream. While the provided research doesn't detail specific new product launches from Apple (APC.F, trading at $226.65 with a market cap of $3.33 trillion), its influence on device roadmaps and user adoption of satellite features is undeniable. The seamless integration of satellite connectivity into standard smartphones, without requiring specialized hardware, is a critical factor for widespread commercial success.

The industry is moving towards a future where users will find it harder to distinguish between terrestrial and non-terrestrial networks (NTNs), with connectivity blending seamlessly between the two. This "invisible" integration is precisely where device manufacturers like Apple hold immense power. Their design choices, software updates, and support for new communication standards, such as 3GPP Release 17 NTN, will dictate how quickly and effectively satellite-to-cell services are adopted by the mass market.

Currently, some devices offer limited satellite-powered texting or emergency SOS features, often through partnerships like Verizon's with Skylo. However, the goal of D2D providers like AST SpaceMobile and Starlink Mobile is to enable full voice, video, and data calls directly to unmodified phones. This requires robust RF and software compatibility within devices, making collaboration with OEMs essential. Apple's historical ability to drive technological adoption and set industry standards means its embrace of advanced satellite capabilities could accelerate the entire sector.

Moreover, as satellite connectivity expands, it creates new opportunities for device-centric services and applications, especially in remote or previously unconnected areas. This could range from enhanced location-based services and IoT connectivity to entirely new categories of mobile experiences. Therefore, while telecom carriers and satellite operators build the infrastructure, it will be the device ecosystem, heavily influenced by players like Apple, that ultimately translates this technological potential into tangible value for consumers and enterprises.

The telecom sector is at an inflection point, with satellite connectivity moving from niche to mainstream. Investors should watch for tangible milestones in satellite deployment, clear revenue-sharing models, and the ability of carriers to translate enhanced coverage into sustained customer loyalty and profitability. The convergence of space and terrestrial networks promises a truly ubiquitous future, but execution and economic hurdles remain significant.

Want deeper research on any stock? Try Kavout Pro for AI-powered analysis, smart signals, and more. Already a member? Add credits to run more research.